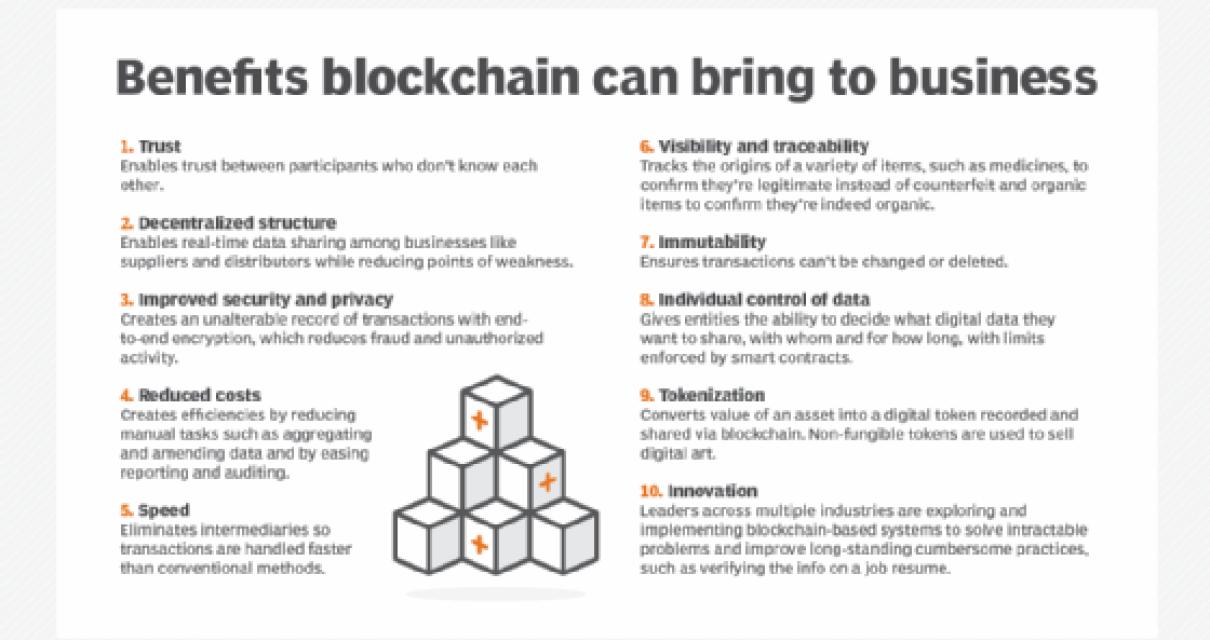

The Benefits of Blockchain Technology

There are many benefits of blockchain technology. Here are a few:

1. Blockchain is secure: A blockchain is secure because it is a distributed ledger that is verified by a network of nodes. Each node stores a copy of the ledger, and requires consensus from the network before changes can be made to it. This makes it difficult for anyone to tamper with the ledger, which makes it a secure technology.

2. Blockchain is transparent: A blockchain is transparent because all transactions and data stored on it are public. This makes it easy for anyone to access and verify information.

3. Blockchain is efficient: A blockchain is efficient because it allows for quick and easy transactions. Because transactions are processed through a network of nodes, there is no need for banks or other third-party institutions to process transactions. This makes it a more efficient way to conduct business.

4. Blockchain is secure and transparent: A blockchain is secure and transparent because it uses cryptography to protect data and transactions from being tampered with. Cryptography is a form of encryption that helps protect information from being accessed by unauthorized individuals. Additionally, the public nature of a blockchain makes it difficult for anyone to hide information from view.

What is Blockchain Technology?

Blockchain technology is an innovative way to create a secure, tamper-proof record of transactions. It works by using a network of participating nodes to create a public ledger of all transactions. This ledger is constantly updated and can be verified by anyone.

The benefits of blockchain technology include:

It is secure: Transactions are verified by multiple nodes and recorded in a public ledger. This makes it difficult for hackers to steal or tamper with data.

Transactions are verified by multiple nodes and recorded in a public ledger. This makes it difficult for hackers to steal or tamper with data. It is transparent: Anyone can view the ledger, so everyone can see who has what and when it was traded. This makes it difficult for people to cheat or skirt the rules.

Anyone can view the ledger, so everyone can see who has what and when it was traded. This makes it difficult for people to cheat or skirt the rules. It is tamper-proof: Nodes can only add new entries to the ledger if they are verified by the network as being accurate. This makes it difficult for anyone to interfere with the record of transactions.

Nodes can only add new entries to the ledger if they are verified by the network as being accurate. This makes it difficult for anyone to interfere with the record of transactions. It is decentralized: Unlike traditional systems, which are controlled by a few centralized entities, blockchain technology is decentralized, meaning that it is not controlled by any one individual or group. This makes it more resistant to cyberattacks and more reliable in terms of accuracy.

Unlike traditional systems, which are controlled by a few centralized entities, blockchain technology is decentralized, meaning that it is not controlled by any one individual or group. This makes it more resistant to cyberattacks and more reliable in terms of accuracy. It is affordable: Blockchain technology is relatively cheap to set up and maintain, making it an affordable option for businesses of all sizes.

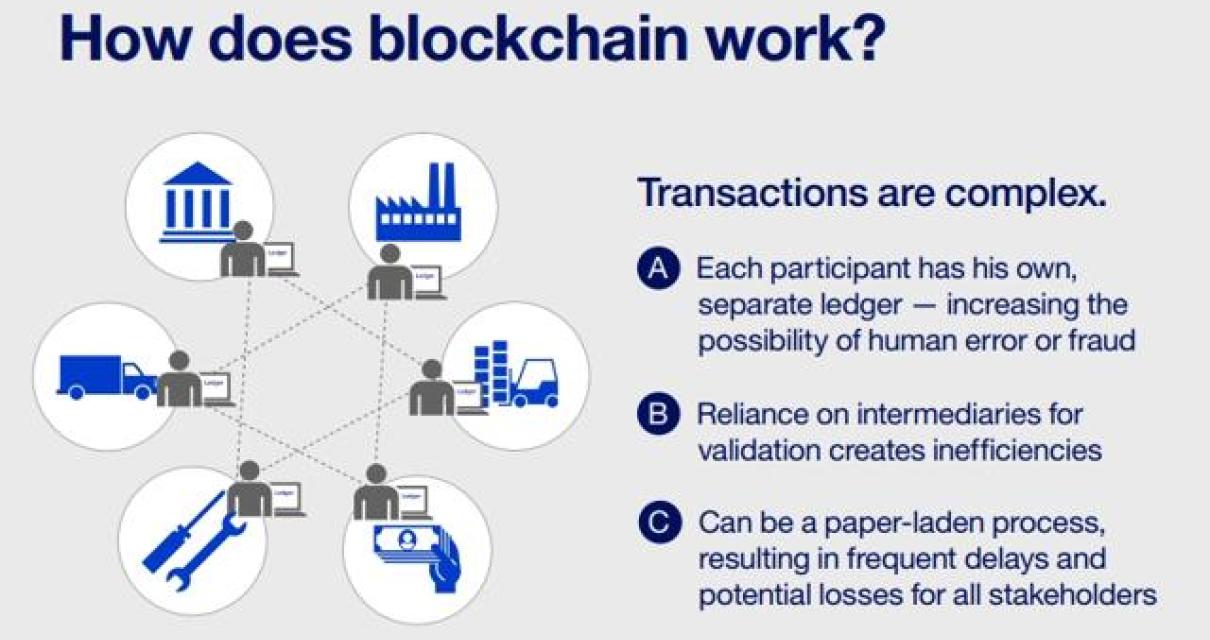

How Does Blockchain Work?

When two people want to trade something, they first need to find a common tradeable currency. For example, if one person wants to trade their car for another person’s bike, they would need to find a common tradeable currency that both parties could use. Once they have found a common currency, they would then need to find a place to trade their goods.

With blockchain technology, this process could be replaced by a digital record of the trade that is stored on a network of nodes. Whenever two people wanted to trade something, they would first need to find each other on the network. Once they had found each other, they would then need to agree on a trade value and complete the trade.

The benefit of using blockchain technology is that it eliminates the need for a third party to facilitate the trade. This means that the trade can take place faster and more securely than with traditional systems. Additionally, because the trade is recorded on a public ledger, anyone can verify that the trade took place and that the values involved were correct.

How Does Blockchain Work?

When a block is added to the blockchain, it is linked to a cryptographic hash of the previous block, creating a chain of blocks. Bitcoin nodes use the block chain to differentiate legitimate Bitcoin transactions from attempts to re-spend coins that have already been spent elsewhere.

Each block contains a cryptographic hash of the block before it, a timestamp, and transaction data. Bitcoin nodes use the block chain to differentiate legitimate Bitcoin transactions from attempts to re-spend coins that have already been spent elsewhere.

Real-World Applications of Blockchain Technology

Some potential real-world applications of blockchain technology include creating a tamper-proof record of ownership for digital assets such as property deeds or securities, tracking the movement of goods and money through supply chains, and conducting secure online voting.

The Future of Blockchain Technology

Blockchain technology is one of the most promising new technologies in the world today. It is a distributed ledger that allows for secure, transparent, and tamper-proof transactions. This technology has the potential to revolutionize many industries, including finance, retail, and supply chains.

The future of blockchain technology looks very promising. It is currently being used by a number of major companies and governments around the world, and there are indications that it will continue to grow in popularity. There are a number of reasons why blockchain technology is so promising.

First, blockchain technology is secure. Unlike traditional systems, which are vulnerable to hackers, blockchain technology is immune to cyberattacks. This is because the entire network is based on a decentralized network of computers, which makes it difficult for anyone to hack into the system.

Second, blockchain technology is transparent. All transactions on the blockchain are visible to everyone on the network, which makes it easier for people to track the flow of money and assets. This is especially valuable in cases where there is a lack of trust between parties.

Third, blockchain technology is tamper-proof. Each block on the blockchain is encrypted, which makes it difficult for anyone to modify or tamper with the information contained within it. This is particularly valuable in cases where there is a need to ensure the accuracy and authenticity of data.

Overall, blockchain technology is very promising and has the potential to revolutionize many industries. It is currently being used by a number of major companies and governments around the world, and there are indications that it will continue to grow in popularity.

The Disadvantages of Blockchain Technology

There are a few disadvantages to using blockchain technology.

First, blockchain technology is slow. Transactions can take minutes or hours to complete, which can be a problem when trying to use it for transactions that need to be completed quickly, like payments.

Second, blockchain technology is not immune to cyberattacks. When a hacker gains access to a blockchain, they can potentially steal or destroy the data stored on it.

Third, blockchain technology is not easily transferable. Because it is a decentralized system, transferring a blockchain from one location to another can be difficult.

Fourth, blockchain technology is not currently accepted by many businesses. Because it is new and complex, many companies are not yet prepared to use it.

Finally, blockchain technology is not without its costs. Because it is a new technology, it can be expensive to implement.

Is Blockchain Technology Secure?

Blockchain technology is secure because it uses a distributed network of computers to create a tamper-proof record of transactions. This system makes it difficult for anyone to tamper with the records, since they would need to access all of the computers on the network.

What Are the Use Cases for Blockchain Technology?

The use cases for blockchain technology are endless, but a few popular examples include:

Asset management: A blockchain can be used to track the ownership of assets, such as property or securities.

A blockchain can be used to track the ownership of assets, such as property or securities. Voting: A blockchain can be used to securely record and track votes in a democracy.

A blockchain can be used to securely record and track votes in a democracy. Transactions: A blockchain can be used to verify and track transactions between two parties.

A blockchain can be used to verify and track transactions between two parties. Health records: A blockchain can be used to securely store health records.

A blockchain can be used to securely store health records. Smart contracts: A blockchain can be used to create smart contracts, which are agreements that are automatically executed when specified conditions are met.

A blockchain can be used to create smart contracts, which are agreements that are automatically executed when specified conditions are met. Identity management: A blockchain can be used to manage identities, such as personal or corporate identities.

How Can Blockchain Be Used to Improve Business?

There are a number of ways in which blockchain technology can be used to improve business. One way is through the use of smart contracts. Smart contracts are contracts between two or more parties that are executed automatically based on certain conditions being met. This can be used to improve efficiency and accuracy in business transactions, as well as to reduce the need for third-party verification.

Another way that blockchain technology can be used to improve business is through the creation of a tamper-proof ledger. A tamper-proof ledger is a digital record of all transactions that takes place within a specific network or system. This can be used to ensure that all data is accurate and tamper-proof, allowing for more secure and efficient business operations.

Finally, blockchain technology can be used to create new business models. For example, blockchain technology could be used to create a new type of financial institution that is more secure and efficient than traditional banks. Or it could be used to create a new type of marketplace that is more transparent and efficient than traditional marketplaces.