How the BTC Blockchain Works

The Bitcoin blockchain is a public ledger of all Bitcoin transactions. Bitcoin nodes use the blockchain to differentiate legitimate Bitcoin transactions from attempts to re-spend coins that have already been spent elsewhere. Bitcoin nodes use the block chain to distinguish legitimate Bitcoin transactions from attempts to re-spend coins that have already been spent elsewhere. Transactions are grouped into blocks, which are then chained together using cryptographic proof-of-work. Each block contains a cryptographic hash of the previous block, a timestamp, and transaction data. Bitcoin nodes use the block chain to verify transactions and to create new blocks. When a node has a new block, it broadcasts it to all other nodes. Nodes use their own data to create their own versions of the block chain, with a different set of transactions. The nodes with the most accurate copies of the block chain are rewarded with new bitcoins.

The Benefits of the BTC Blockchain

There are many benefits of using the Bitcoin blockchain technology. Some of the benefits include:

Security: The Bitcoin blockchain is incredibly secure because it is decentralized and has a Proof-of-Work algorithm. This makes it difficult for anyone to tamper with the data.

Fraud Prevention: The Bitcoin blockchain is also used to prevent fraud. For example, when a purchase is made, the blockchain is used to track the transaction and ensure that it occurred as planned. This prevents fraudsters from stealing money or goods.

Transaction Speed: The Bitcoin blockchain is able to process transactions quickly and accurately. This is because it is a distributed system, meaning that there is no central authority that can slow down or stop the transaction.

Transparency: The Bitcoin blockchain is transparent, which means that everyone can see all of the transactions that have taken place. This is helpful in preventing fraud and ensuring that people are not being cheated.

Trust: The Bitcoin blockchain is highly trusted because it is based on a trustless system. This means that people can trust that the data is accurate and that transactions are taking place as planned.

Low Cost: The Bitcoin blockchain is low cost because it does not require a lot of resources to run. This makes it ideal for use in small businesses and other organizations that do not have a lot of money to spend on technology.

The Use Cases of the BTC Blockchain

There are many potential ways in which the BTC blockchain could be used. Here are a few examples:

1. securely storing digital assets

2. tracking ownership of digital assets

3. issuing and managing digital assets

4. conducting transactions with digital assets

5. voting with digital assets

6. holding funds in a safe and secure manner

7. ensuring transparency and trust in digital transactions

The Advantages of the BTC Blockchain

Bitcoin is an innovative payment network and a new kind of money. It is a decentralized digital asset. Transactions are verified by network nodes through cryptography and recorded in a public distributed ledger called a blockchain. Bitcoin is unique in that there are a finite number of them: 21 million.

Bitcoin has several advantages over traditional payment networks. These include:

-No intermediaries: Bitcoin transactions are verified by network nodes directly, without the need for third-party financial institutions. This eliminates the need for costly and time-consuming verification processes and makes it more secure.

-Low cost and fast transactions: Bitcoin transactions are cheaper and faster than traditional payments systems.

-No central control: Bitcoin is decentralized, meaning that there is no central authority or party that can control or manipulate the currency. This makes it immune to political or economic pressures.

-Transparency: All Bitcoin transactions are public and transparent. This makes it easier for people to understand and track the flow of money.

The Disadvantages of the BTC Blockchain

There are some disadvantages to the Bitcoin blockchain technology. Some of these disadvantages include:

1. Scalability: The Bitcoin blockchain is not scalable and can not handle a large number of transactions. This is due to the fact that the blockchain is based on a distributed ledger system, which means that each node must keep track of every transaction. As a result, the blockchain can only handle a limited number of transactions per second.

2. Security: The Bitcoin blockchain is not secure because it is not centralized. This means that there is no single point of control and no one can guarantee the security of the Bitcoin blockchain. This vulnerability has led to the theft of millions of dollars worth of Bitcoin over the past few years.

3. Cost: The Bitcoin blockchain is expensive to use because it requires a lot of resources, such as computer power and storage space. This makes it difficult for small businesses and individuals to use the Bitcoin blockchain.

4. Inefficiency: The Bitcoin blockchain is inefficient because it is slow and it can be difficult to verify transactions. This makes it difficult for businesses to use the Bitcoin blockchain for transactions.

5. Volatility: The Bitcoin blockchain is volatile because the value of Bitcoin can change rapidly, making it difficult for businesses to plan their budgets around the price of Bitcoin.

The Pros and Cons of the BTC Blockchain

There are pros and cons to the Bitcoin blockchain, just as there are to any other type of blockchain technology.

Some pros of the Bitcoin blockchain include that it is a distributed ledger that is transparent and immutable. This means that all transactions on the blockchain are public and can be verified by anyone. Additionally, the Bitcoin blockchain is resistant to modification or alteration.

On the other hand, some cons of the Bitcoin blockchain include that it is an expensive and resource-intensive platform to operate, and it is not well suited for large-scale transactions. Additionally, the Bitcoin blockchain is not suitable for use in mainstream applications yet.

What is a Bitcoin Block?

A Bitcoin block is a data structure that stores transactions and other data related to the Bitcoin network. Blocks are created every 10 minutes, and each block includes a cryptographic hash of the previous block, a transaction list, and a nonce.

What is a Bitcoin Chain?

A Bitcoin chain is a public ledger of all Bitcoin transactions. It is constantly growing as "completed" blocks are added to it with a new set of recordings. Each block contains a cryptographic hash of the previous block, a timestamp, and transaction data. Bitcoin nodes use the block chain to distinguish legitimate Bitcoin transactions from attempts to re-spend coins that have already been spent elsewhere.

What is a Bitcoin Miner?

A Bitcoin miner is a computer process that helps verify and secure Bitcoin transactions by running complex algorithms. Bitcoin miners are rewarded with bitcoin for their efforts.

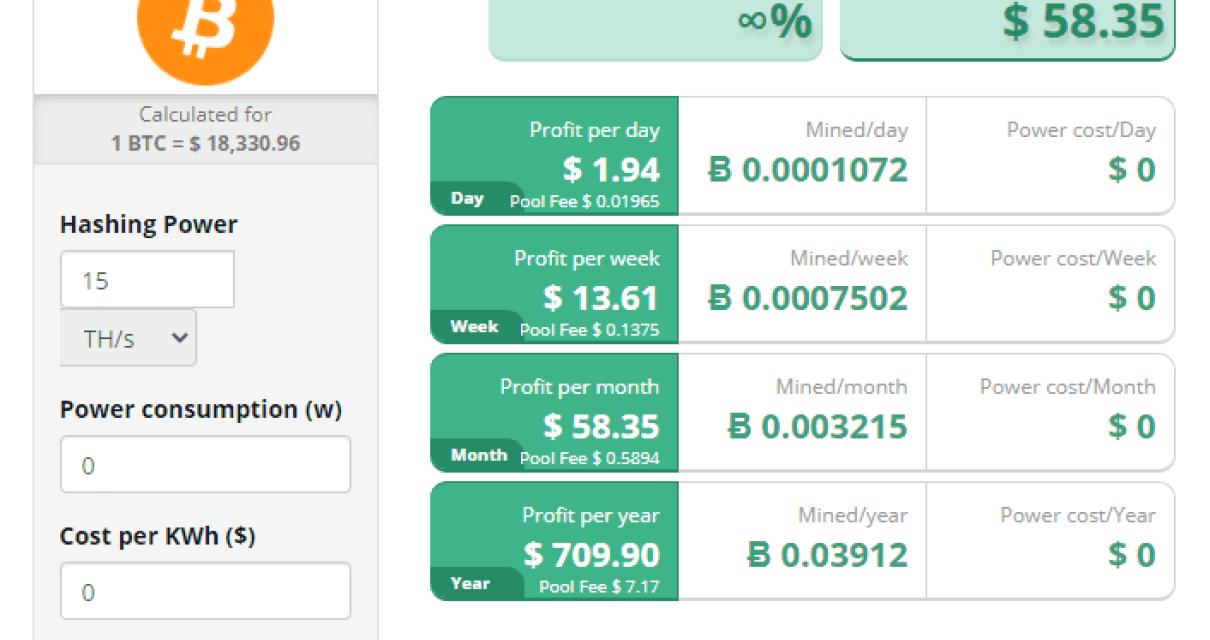

What is Bitcoin Mining?

Bitcoin mining is the process of confirming bitcoin transactions and adding them to the blockchain. Bitcoin mining is done by running powerful computers (known as mining rigs) that race against other mining rigs to solve complex math problems. The first miner to solve the problem and confirm the transaction is rewarded with newly created bitcoins. Bitcoin mining is competitive and today can only be done by people with high-end computer hardware and a lot of electricity.

How Does Bitcoin Mining Work?

Bitcoin mining is the process of verifying and accepting bitcoin transactions and creating new bitcoin. Bitcoin miners are rewarded with transaction fees and newly created bitcoins.

Who Created Bitcoin?

Bitcoin was created by an unknown person or group of people under the name Satoshi Nakamoto. There is no one definitive answer to this question.