Bitcoin and Blockchain: A Love Story

Bitcoin and blockchain technology have been intertwined since the early days of the cryptocurrency. Bitcoin was the first blockchain application, and blockchain technology underpins the decentralized nature of bitcoin.

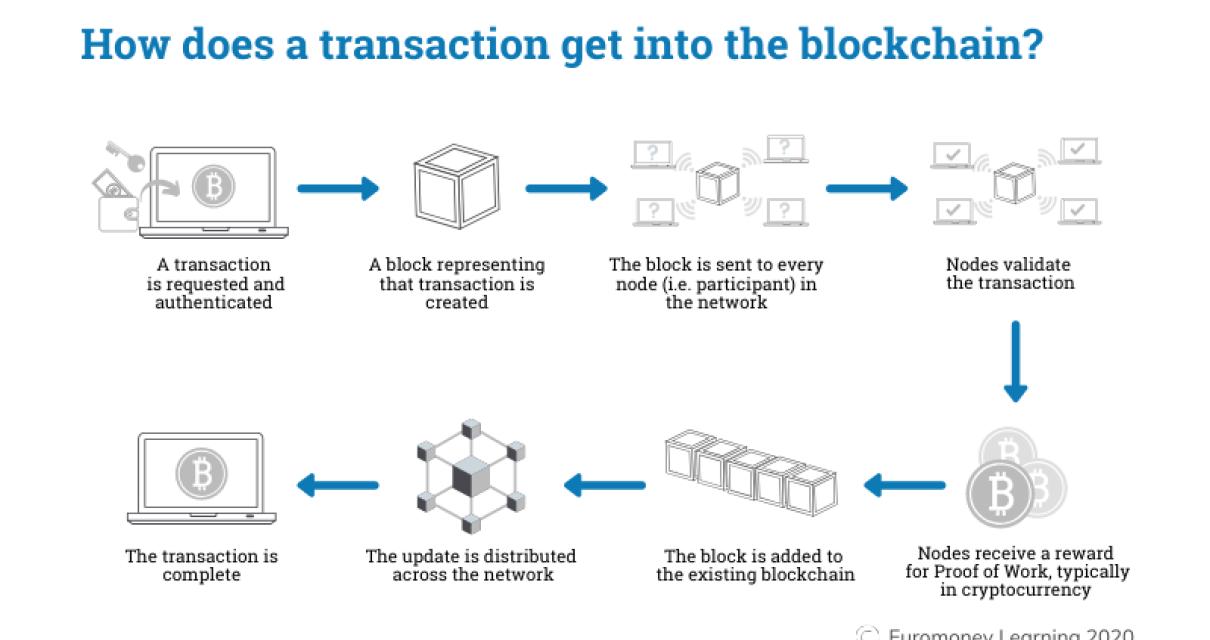

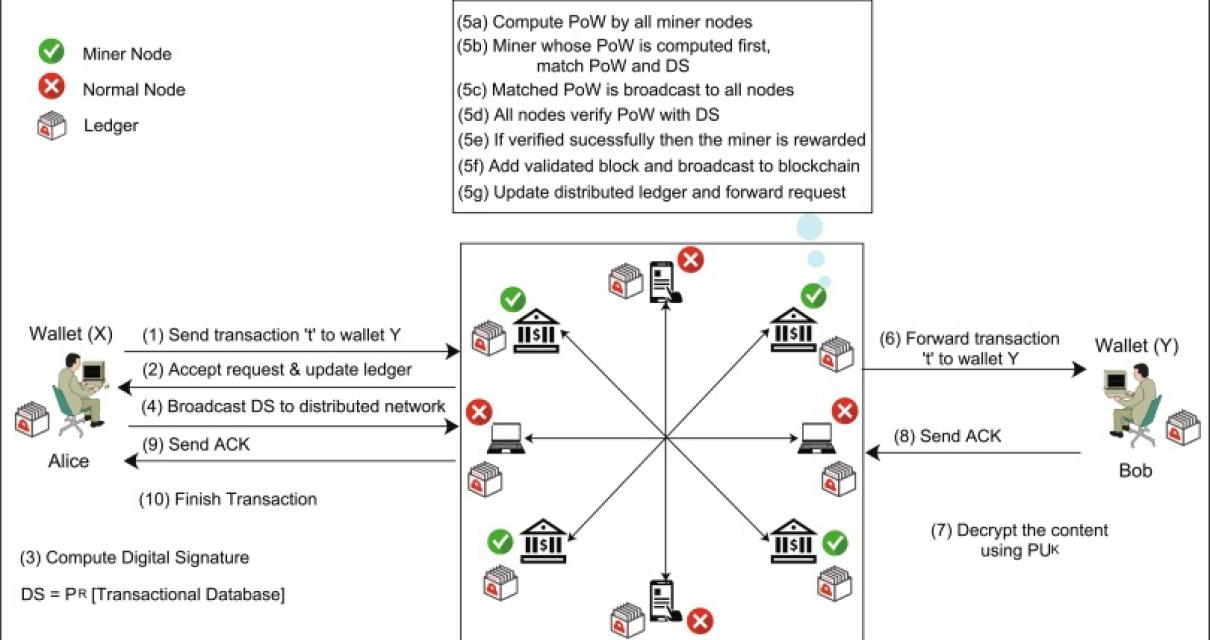

Blockchain technology is a distributed ledger that allows for secure, transparent, and tamper-proof transactions. Transactions are verified by network nodes through cryptography and recorded in a public distributed ledger called a blockchain. Bitcoin and other cryptocurrencies are based on blockchain technology.

Bitcoin was created in 2009 by an unknown person or group of people under the name Satoshi Nakamoto. Bitcoin is pseudonymous, meaning that its creator(s) are not known. Bitcoins are created as a reward for a process known as mining. They can be exchanged for other currencies, products, and services.

In February 2014, Bitcoin reached a all-time high of over $1,200. In March 2017, Bitcoin reached $20,000 for the first time. As of January 2018, Bitcoin is worth over $8,000.

Bitcoin and Blockchain: A Marriage of Convenience

Bitcoin and blockchain technology offer a marriage of convenience, making it easier for people to transact and exchange goods and services.

Bitcoin is a digital currency that uses cryptography to secure its transactions and to control the creation of new units. Transactions are verified by network nodes through cryptography and recorded in a public dispersed ledger called a blockchain. Bitcoin is unique in that there is a finite number of them: 21 million.

Blockchain technology allows for secure, transparent and tamper-proof transactions. It also allows for payments to be made without intermediaries such as banks. Transactions are tracked on a public ledger and made available to all network participants.

Bitcoin and blockchain technology have been praised for their ability to improve trust and security, reduce costs and increase efficiency in transactions. They have also been criticized for their volatility, scalability limitations and lack of mainstream acceptance.

Bitcoin and Blockchain: A Tale of Two Technologies

Bitcoin and Blockchain are two of the most popular technologies in the world today. They are both cutting edge and have the potential to change the way the world works. However, they also have some key differences that can affect how well they work together.

Bitcoin is a digital asset and blockchain is the underlying technology that makes it possible. Bitcoin is a currency that is created and used on a peer-to-peer network. Transactions are verified by network nodes and recorded in a public distributed ledger called a blockchain. Bitcoin is unique in that there is only a finite number of them: 21 million.

Blockchain is a distributed database that allows for secure, transparent and tamper-proof transactions. It works as a distributed ledger, allowing parties to exchange information without the need for a third party. Transactions are verified by network nodes and recorded in blocks. Each block contains a cryptographic hash of the previous block, a timestamp, and transaction data.

Bitcoin and Blockchain have different characteristics that can affect their ability to work together. Bitcoin is faster and more reliable than blockchain, but it is not immune to fraud or cyberattacks. Blockchain is more secure than bitcoin, but it can take longer to process transactions.

Overall, Bitcoin and Blockchain have a lot of potential, but they will need to work better together if they want to become mainstream technologies.

Bitcoin vs. Blockchain: The Battle for supremacy

Bitcoin and blockchain are two of the most popular digital currencies in the world. They both have their own strengths and weaknesses, but which one is better?

Bitcoin

Bitcoin is the original and most well-known cryptocurrency. It was created in 2009 by an anonymous person or group known as Satoshi Nakamoto. Bitcoin is decentralized, meaning there is no government or central authority that regulates it. This makes it a more secure and trustless currency than traditional ones.

One of the main advantages of Bitcoin is its simplicity. Unlike other cryptocurrencies, Bitcoin doesn't require a complex set of rules or advanced technology to operate. You can simply download the Bitcoin wallet app and start receiving payments.

Another advantage of Bitcoin is its low processing fees. Many online merchants now accept Bitcoin as payment, which helps to increase its popularity.

However, one of the main drawbacks of Bitcoin is its limited supply. There will only ever be 21 million Bitcoins available, which means it's not suitable for everyday use.

Blockchain

Blockchain is a distributed database that allows for secure and transparent transactions. It was first conceptualized in 2009 by an anonymous person or group known as Satoshi Nakamoto.

Unlike Bitcoin, blockchain is not decentralized. Instead, it is based on a peer-to-peer network where all nodes are connected. This makes it more reliable and secure than Bitcoin, as it eliminates the possibility of a single party controlling the data.

One of the main advantages of blockchain is its tamper-proof feature. This means that it is impossible for anyone to tamper with transactions or data stored on the blockchain. This makes it ideal for use in financial transactions, as it eliminates the risk of fraud.

Another advantage of blockchain is its ability to handle large volumes of transactions. Unlike Bitcoin, which can only handle around seven transactions per second, blockchain can handle tens of thousands of transactions per second. This makes it perfect for use in mainstream businesses.

However, one of the main drawbacks of blockchain is its high fees. Fees can be expensive, which makes it unsuitable for small transactions. Additionally, blockchain is still in its early stages and there are some security issues that need to be addressed.

Bitcoin or Blockchain: Which is the better investment?

Bitcoin and blockchain are two different technologies with different purposes. Bitcoin is a digital currency that uses blockchain technology to facilitate transactions. Blockchain is a distributed database that allows for secure, transparent and tamper-proof transactions. While both technologies have potential benefits, it is important to consider the specific uses of each before making a decision.

Bitcoin and Blockchain: The perfect storm

As a society, we’re constantly looking for new and innovative ways to improve our lives. This is especially true when it comes to technology, as we strive to find solutions that can make our lives easier and more efficient.

Bitcoin and blockchain technology are two such solutions that have the potential to revolutionize the way we do business and interact with the world around us.

What is Bitcoin?

Bitcoin is a digital asset and a payment system invented by an unknown person or group of people under the name Satoshi Nakamoto. Bitcoin is based on a blockchain, a distributed database that allows for secure, anonymous transactions.

How does Bitcoin work?

When you want to buy something with Bitcoin, you first need to create a digital “wallet.” This wallet is where you store your Bitcoin and any other cryptocurrencies you may own.

To use Bitcoin, you send your Bitcoin to someone else’s digital wallet. They then use that Bitcoin to purchase something from a merchant.

What is blockchain?

A blockchain is a distributed database that allows for secure, anonymous transactions. Transactions are added to a blockchain in a chronological order and can be seen by everyone.

Why is blockchain important?

Blockchain is important because it eliminates the need for a third party to verify transactions. This is why it’s often used in cryptocurrency transactions.

How is blockchain used in Bitcoin and other cryptocurrencies?

When you want to buy something with Bitcoin or another cryptocurrency, you first need to create a digital “wallet.” This wallet is where you store your Bitcoin or other cryptocurrencies.

To use Bitcoin or another cryptocurrency, you send your Bitcoin or other cryptocurrencies to someone else’s digital wallet. They then use that Bitcoin or other cryptocurrencies to purchase something from a merchant.

What are the benefits of using Bitcoin and blockchain?

There are many benefits to using Bitcoin and blockchain technology. These benefits include:

1. Security: Bitcoin and blockchain technology are extremely secure. This is because they use a blockchain, which is a distributed database that allows for secure, anonymous transactions.

2. Transparency: Bitcoin and blockchain technology are transparent. This means everyone can see how many Bitcoins or other cryptocurrencies each person has. This is important because it allows for transparency in the financial system.

3. Ease of use: Bitcoin and blockchain technology are easy to use. This is because they are digital assets and payment systems that are based on a blockchain.

Bitcoin and Blockchain: A symbiotic relationship

Bitcoin and blockchain are two of the most important inventions in all of history. They are a symbiotic relationship, where each helps the other grow and improve.

Bitcoin is the original and most well-known blockchain technology. It allows people to conduct transactions and store data without needing a central authority. Bitcoin is also decentralized, meaning it is not controlled by a single entity.

Blockchain is the underlying technology that powers Bitcoin and other cryptocurrencies. It is a distributed ledger that allows for secure, transparent transactions. It is also incorruptible, meaning it cannot be tampered with or reversed.

Together, Bitcoin and blockchain are changing the world for the better. They are creating a more equitable and transparent society, and they are revolutionizing the way we do business.

Bitcoin and Blockchain: Complementary technologies

Bitcoin and blockchain technology are complementary technologies. They both can help solve certain problems and improve efficiencies in different industries.

Bitcoin is a digital asset and a payment system invented by Satoshi Nakamoto. It is based on a decentralized database. Transactions are verified by network nodes through cryptography and recorded in a public distributed ledger called a blockchain. Bitcoin is unique in that there are a finite number of them: 21 million.

Blockchain is a distributed database that allows for transparent, secure and tamper-proof transactions. It is used to track the ownership of digital assets, to prevent fraud, to manage contracts and to create a transparent record of all digital transactions.

Together, they can help reduce costs and increase efficiency in many industries. For example, the use of blockchain could help improve the security and trustworthiness of online transactions. It could also help reduce the time it takes to process transactions and make them more transparent.

Bitcoin and blockchain technology are still relatively new and their potential applications are still being explored. As their popularity grows, so too will their impact on various industries.

Bitcoin plus Blockchain equals success

Bitcoin and blockchain technology are two of the most important innovations in digital history. They are creating a new way of doing business, and they are changing the way we live our lives.

Bitcoin and blockchain technology are creating a new way of doing business

Bitcoin and blockchain technology are revolutionising how we do business. They are creating a new way of transferring money, and they are changing the way we do business.

Bitcoin and blockchain technology are changing the way we live our lives

Bitcoin and blockchain technology are changing the way we live our lives. They are creating a new global economy, and they are changing the way we do business.

How Bitcoin and Blockchain are changing the financial landscape

Bitcoin and blockchain technology are changing the financial landscape by creating a new way to handle transactions. Bitcoin and blockchain are decentralized systems that allow for secure transactions without the need for a third party.

Bitcoin and blockchain are both examples of distributed ledgers. A distributed ledger is a digital record of transactions that is shared among a network of computers. Transactions are verified and recorded in a public ledger. This makes it impossible for anyone to fraudulent transactions.

Bitcoin and blockchain are also examples of digital currencies. Digital currencies are systems that use cryptography to secure their transactions and to control the creation of new units. Bitcoin is the first and most well-known digital currency.

Bitcoin and blockchain are still in their early stages of development. There are still many questions that need to be answered about how they will change the financial landscape. However, there is no doubt that they are changing the way we think about money and transactions.

The future of finance: Bitcoin, blockchain and beyond

According to a study by PwC, the future of finance is blockchain. The study found that blockchain could play a role in improving the transparency and efficiency of transactions, reducing costs and making it easier for companies to do business with each other.

Bitcoin and blockchain are two key aspects of the future of finance. Bitcoin is a digital currency that uses blockchain technology to secure transactions and track ownership. Blockchain is a distributed database that allows for transparent, secure and tamper-proof transactions.

Other key aspects of the future of finance include artificial intelligence (AI) and machine learning. AI is able to process large amounts of data quickly and make complex decisions. Machine learning is a type of AI that can learn from data and improve over time.

Overall, the future of finance looks promising. Blockchain and other technologies are helping to improve the transparency, security and efficiency of transactions.