The Benefits of Smart Contracts on the Blockchain

Smart contracts are a way to make agreements between parties more efficient and reliable. They can be used for a variety of purposes, such as property transactions, bank loans, and insurance policies.

They are also a way to reduce the risk of fraud and cybercrime. Because smart contracts are automatically executed when specific conditions are met, there is no need for third parties to verify the contract. This means that there is less chance of fraud or error.

Smart contracts also have other benefits. For example, they can reduce the time it takes to complete a transaction. And they can ensure that all parties involved in a transaction are aware of the terms of the agreement. This makes it easier for them to comply with the terms of the contract.

Overall, smart contracts are a useful tool for businesses and individuals. They can help to speed up the process of making agreements, reduce the risk of fraud, and ensure that all parties involved in a transaction are aware of the terms of the agreement.

How Smart Contracts Can Help Businesses Streamline Operations

Smart contracts can help businesses streamline operations by automating certain business processes. For example, a business could use a smart contract to automatically pay its employees every week. This would save the business time and money, and would ensure that employees are paid on time.

Other examples of how smart contracts can help businesses streamline operations include:

automating purchasing and shipping processes

managing inventory and delivery schedules

automating billing and invoicing

automating payroll and employee benefits

These are just a few examples of how smart contracts can be used to streamline business operations. There are many other possibilities, so it is important to explore what is possible before making any decisions.

What is the Best Blockchain for Smart Contracts?

There is no single “best” blockchain for smart contracts, as the best blockchain for a particular use case may vary depending on the specific requirements of that use case. Some of the more popular blockchains for smart contracts include Ethereum, Bitcoin, and Litecoin.

How Smart Contracts Work on the Blockchain

Smart contracts are digital contracts between two or more parties that are executed by the blockchain. They are self-executing and self-enforcing. This means that once a smart contract is created, it will automatically execute the terms of the agreement between the parties without any need for third party intervention.

A key feature of smart contracts is that they are tamper-proof. This means that they cannot be altered or tampered with once they have been created, which makes them a very secure way to execute an agreement.

Smart contracts can also be used to create a trustless system. This means that parties can trust that the terms of a contract will be carried out as agreed, without needing to rely on any third party verification.

Smart contracts can also be used to create a transparent system. This means that everyone involved in a contract can see the terms and conditions of the agreement, which makes it easier to resolve any disputes.

Finally, smart contracts can be used to automate transactions. This means that they can be used to automate the process of completing an agreement between two or more parties, which can save time and money.

The Benefits of Using Smart Contracts

There are a number of benefits to using smart contracts. Some of the benefits include:

1. Increased Efficiency – Smart contracts allow for increased efficiency because they automate many of the processes involved in a transaction. This can save both time and money for both parties involved in the transaction.

2. Reduced Errors – Because smart contracts are automated, they reduce the chances of errors. This means that both parties involved in a transaction can be sure that the details of the deal are accurate and that there are no potential complications down the line.

3. Increased Trust – By using smart contracts, both parties involved in a transaction can have increased trust in each other. This is because there is a clear record of the deal being made and no chance of disputes later on.

4. Reduced Costs – Smart contracts can also reduce costs associated with transactions. This is because they can reduce the need for third-party involvement or paperwork.

5. Increased Security – Smart contracts are also incredibly secure. This is because they are programmed to follow specific rules and cannot be easily altered or tampered with. This makes them a safe way to conduct transactions

How Smart Contracts Can Be Used to Automate Business Processes

A smart contract is a type of contract that is executed and enforced by a computer system. In a smart contract, all the terms of the contract are encoded in code, which is then stored on a blockchain. When a party to the contract wants to perform its obligations, it accesses the code and uses it to execute the agreed-upon actions.

This technology can be used to automate business processes. For example, a company could use a smart contract to automate the process of issuing shares. The contract would contain all the information necessary to issue the shares, including the price and quantity. Once the contract is signed by all parties, the computer system would automatically execute the instructions and issue the shares.

This technology can also be used to automate the contracting process. For example, a company could use a smart contract to automate the process of bidding on contracts. The contract would contain all the information necessary to submit a bid, including the price and quantity. Once the contract is signed by all parties, the computer system would automatically execute the instructions and award the contract to the bidder with the lowest bid.

Smart contracts have many other applications, including the automating of financial transactions and the execution of contracts between strangers. As smart contracts become more widely used, they may play an even larger role in automating business processes.

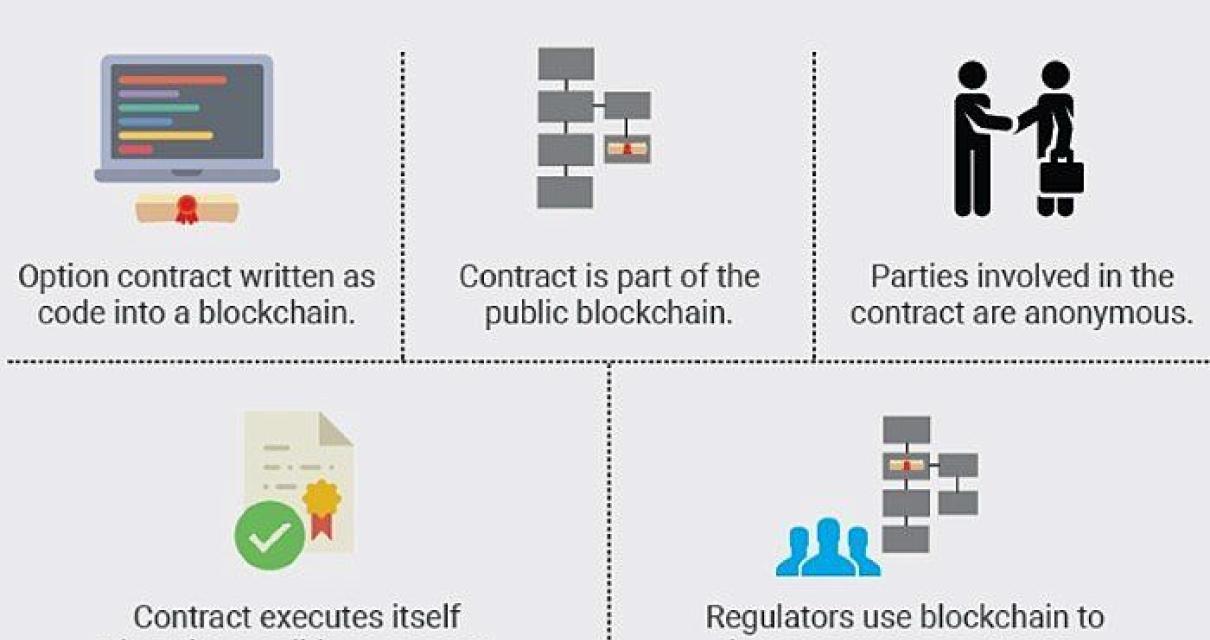

What is a Smart Contract and How Does it Work?

A Smart Contract is a contract that is executed by computer code. The code is stored on a blockchain, which is a public ledger of all cryptocurrency transactions. It allows two parties to make a contract without the need for a third party. The code is automatically executed when specific conditions are met.

How to Use Smart Contracts in Your Business

There are a few ways in which you can use smart contracts in your business. They can be used to create legally-binding contracts, to manage and track assets, to automate payments, and to enable peer-to-peer transactions.

1. Use Smart Contracts to Create Legally-Binding Contracts

Smart contracts can be used to create legally-binding contracts. This can be useful for a number of reasons, including reducing the need for paperwork, ensuring that contract terms are enforced, and protecting businesses from fraudulent behaviour.

2. Use Smart Contracts to Manage and Track Assets

Smart contracts can also be used to manage and track assets. This can be useful for a number of reasons, including reducing the need for paperwork, ensuring that assets are properly accounted for, and protecting businesses from fraudulent behaviour.

3. Use Smart Contracts to Automate Payments

Smart contracts can also be used to automate payments. This can be useful for a number of reasons, including reducing the need for paperwork, ensuring that payments are made on time, and protecting businesses from fraudulent behaviour.

4. Use Smart Contracts to Enable Peer-to-Peer Transactions

Smart contracts can also be used to enable peer-to-peer transactions. This can be useful for a number of reasons, including reducing the need for paperwork, ensuring that transactions are secure, and protecting businesses from fraudulent behaviour.

What are the Advantages of Smart Contracts?

There are many advantages to using smart contracts, including:

-They are secure: Smart contracts are designed to be secure, meaning that they cannot be altered or hacked.

-They are transparent: Smart contracts are transparent, meaning that everyone involved in the contract can see what is happening.

-They are efficient: Smart contracts are efficient, meaning that they can be executed quickly and without error.

-They are cost-effective: Smart contracts are cost-effective, meaning that they can save money on costs associated with traditional contracts.

How Do Smart Contracts Work?

Smart contracts are computer protocols that facilitate, verify, and enforce the negotiation and performance of a contract. They are built on blockchain technology and use a distributed database to manage a contract’s terms.

When two parties enter into a contract, they create an agreement that is encoded in a digital format. The terms of the contract are automatically tracked and verified through the use of blockchain technology. Once the terms of the contract have been verified, the contract is executed by both parties.

Smart contracts allow for a trustless and secure environment, as both parties are able to verify the terms of the contract without third-party involvement. They also allow for the automatic performance of a contract, eliminating the need for intermediaries.

What are the Benefits of Using a Blockchain for Smart Contracts?

There are a number of benefits to using a blockchain for smart contracts. These benefits include:

1. Increased Security: A blockchain is a distributed ledger that is secure by design. This means that it is impossible for one party to tamper with the data.

2. Improved Transparency: A blockchain is transparent, which means that all participants can see the transactions and information that is being stored. This makes it easier for people to trust the system.

3. Reduced Costs: A blockchain is decentralized, which means that there is no central authority that can control the network. This reduces the costs associated with operating a smart contract platform.

4. Increased Speed: A blockchain is a distributed network, which means that it can process transactions quickly. This makes it ideal for use in smart contracts.

5. Reduced Risk: A blockchain is a tamper-proof system, which means that it is difficult for hackers to access the data. This reduces the risk of fraud in smart contracts.