What is a blockchain in cryptocurrency?

A blockchain is a decentralized digital ledger of all cryptocurrency transactions. It is constantly growing as "completed" blocks are added to it with a new set of recordings. Each block contains a cryptographic hash of the previous block, a timestamp, and transaction data. Bitcoin nodes use the block chain to distinguish legitimate Bitcoin transactions from attempts to re-spend coins that have already been spent elsewhere.

The basics of blockchain technology

A blockchain is a distributed database that can be used to track the ownership of digital assets. It works by building a chain of blocks, each block containing a timestamp and a link to the previous block. This allows users to transparently see the history of transactions.

How does blockchain work?

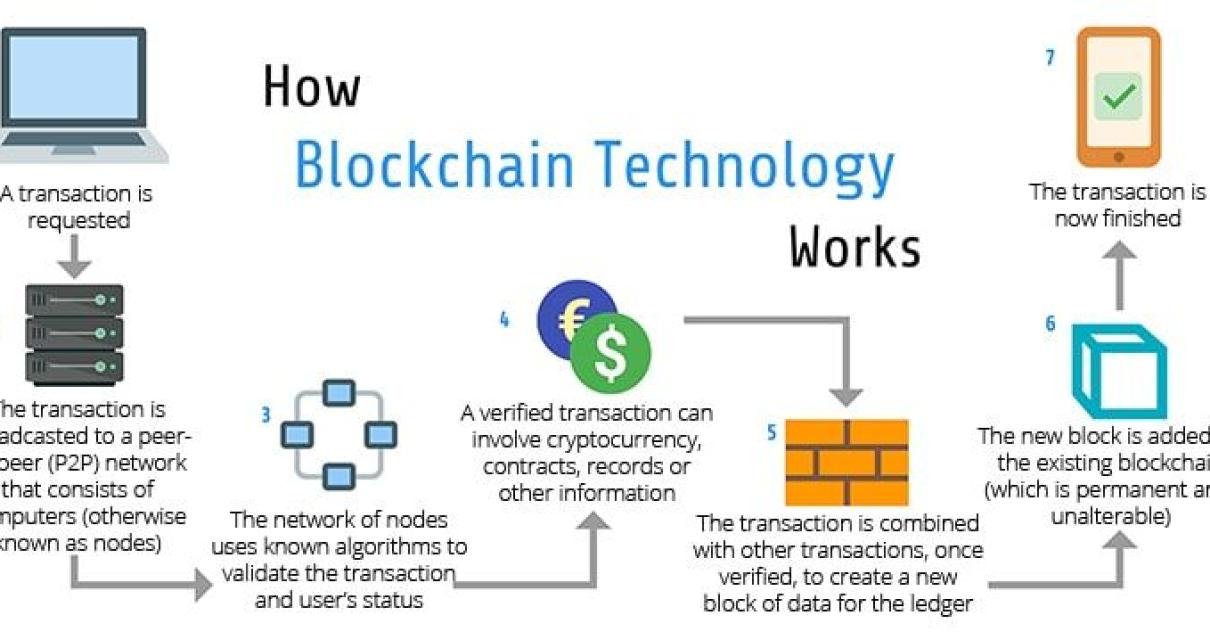

The blockchain works by distributing a copy of the database to every participant in the network. Whenever a new block is added to the chain, all of the nodes in the network check to see if the block is legitimate and then add it to their copy of the ledger. Once a block has been added to the chain, it is difficult to change.

What are the benefits of blockchain technology?

The benefits of blockchain technology include:

-Transparency: The blockchain is transparent, meaning everyone can see the history of transactions.

- Immutability: The blockchain is immutable, meaning it is impossible to change or remove any data once it has been added to the chain.

- Security: The blockchain is secure, meaning it is difficult to tamper with or corrupt data.

- Scalability: The blockchain is scalable, meaning it can handle a large number of transactions.

How does a blockchain work?

A blockchain is a digital ledger of all cryptocurrency transactions. It is constantly growing as “completed” blocks are added to it with a new set of recordings. Each block contains a cryptographic hash of the previous block, a timestamp, and transaction data. Bitcoin nodes use the block chain to differentiate legitimate Bitcoin transactions from attempts to re-spend coins that have already been spent elsewhere.

The history of blockchain technology

Blockchain technology is a distributed ledger technology that was first proposed in 2008 by an anonymous person or group of people under the name Satoshi Nakamoto.

The idea behind blockchain technology is to create a tamper-proof, encrypted database of all cryptocurrency transactions. This database is decentralized, meaning that it is not controlled by any single entity.

Instead, the blockchain is controlled by a network of computers spread across the globe. This makes it difficult for anyone to tamper with the data.

A key feature of blockchain technology is that it allows for the secure transmission of data between two parties without the need for a third party, such as a bank.

This allows for a wide range of applications, including the tracking of goods and the validation of digital contracts.

Bitcoin and blockchain technology

Bitcoin is a digital asset and a payment system invented by Satoshi Nakamoto. Transactions are verified by network nodes through cryptography and recorded in a public dispersed ledger called a blockchain. Bitcoin is unique in that there are a finite number of them: 21 million.

A blockchain is a continuously growing list of records, called blocks, which are linked and secured using cryptography. Each block contains a cryptographic hash of the previous block, a timestamp, and transaction data. Bitcoin nodes use the block chain to distinguish legitimate Bitcoin transactions from attempts to re-spend coins that have already been spent elsewhere.

Bitcoin is created as a reward for a process known as mining. Miners are rewarded with bitcoin for verifying and committing transactions to the blockchain. Bitcoin can also be exchanged for other currencies, products, and services. As of February 2015, over 100,000 merchants and vendors accepted bitcoin as payment.

The future of blockchain technology

Blockchain technology is still in its early stages, but it has the potential to revolutionize many industries. Some of the most promising applications of blockchain technology include:

Financial services

The potential for blockchain technology in the financial sector is vast. The technology could be used to create a tamper-proof record of financial transactions, allow for faster and more secure transactions, and reduce the costs associated with traditional banking systems.

Industries such as shipping and logistics

Blockchain technology could be used to create a tamper-proof record of shipping and logistics transactions. This would help to ensure that items are delivered to their destination safely and without any delays.

Government

Blockchain technology has the potential to help governments to carry out transactions more efficiently and transparently. This could help to reduce the costs associated with government agencies, and also make it easier for citizens to interact with their government.

Education

Blockchain technology could be used to create a tamper-proof record of academic transactions. This would make it easier for students to track their progress throughout their education, and also reduce the amount of time that is needed to process academic paperwork.

Ethereum and blockchain technology

Ethereum is a decentralized platform that runs smart contracts: applications that run exactly as programmed without any possibility of fraud or third party interference. Ethereum is a decentralized platform that runs smart contracts: applications that run exactly as programmed without any possibility of fraud or third party interference. Ethereum is a decentralized platform that runs smart contracts: applications that run exactly as programmed without any possibility of fraud or third party interference. Ethereum is a decentralized platform that runs smart contracts: applications that run exactly as programmed without any possibility of fraud or third party interference.

Initial coin offerings and blockchain technology

Blockchain technology is often associated with initial coin offerings (ICOs), which are a type of crowdfunded venture capital. ICOs are a way for startups to raise money by issuing their own digital tokens. These tokens can be used to purchase goods or services from the startup’s platform.

The popularity of ICOs has led to a surge in blockchain technology adoption. Many large companies, such as IBM and Microsoft, are now investing in blockchain technology to help them better understand the technology. This interest has led to a proliferation of blockchain-based projects.

Smart contracts and blockchain technology

A blockchain is a digital ledger of all cryptocurrency transactions. It is constantly growing as “completed” blocks are added to it with a new set of recordings. Each block contains a cryptographic hash of the previous block, a timestamp, and transaction data. Bitcoin nodes use the block chain to differentiate legitimate Bitcoin transactions from attempts to re-spend coins that have already been spent elsewhere.

A “smart contract” is a contract that is intelligently executed by a computer network. A smart contract uses blockchain technology to create legal agreements between parties that are enforced by blockchain code. These agreements are often more binding and efficient than traditional contracts because they are recorded on a public blockchain and are not subject to revision or dispute.

Blockchain technology has the potential to revolutionize many industries, including finance, law, and governance. It could help to improve trust and transparency in these industries, reduce costs and delays, and create new opportunities for innovation.

Decentralized applications and blockchain technology

Decentralized applications and blockchain technology are two of the most revolutionary technologies in the world today. They have the potential to completely change the way we do business and interact with the world around us.

A decentralized application is an app that runs on a network of computers rather than on a single server. This means that the app is decentralized, meaning that it is not controlled by any one person or organization.

Blockchain technology is the platform on which these decentralized applications are built. It is a distributed ledger system that allows for secure, transparent and tamper-proof transactions.

The potential benefits of using decentralized applications and blockchain technology are endless. They could revolutionize the way we do business, make it easier to conduct transactions and help to increase security and transparency.

Blockchain technology and the law

Blockchain technology and the law is a new research area that investigates the potential legal effects of blockchain technology. The study of blockchain technology and the law has the potential to provide insights into a range of legal issues, including digital rights management, intellectual property, and cybersecurity.

One of the key benefits of studying blockchain technology and the law is that it could help to improve the understanding of how blockchain technology works and how it could be used in the future. This could help to improve the security and reliability of blockchain technology and help to ensure that it is used in a responsible way.

Another benefit of studying blockchain technology and the law is that it could help to improve the understanding of how digital rights management works. This could help to ensure that individuals have the rights that they are entitled to under the law, including the right to privacy.

Study of blockchain technology and the law could also have implications for the way that intellectual property is protected. This could help to protect the rights of creators of intellectual property, and it could also help to ensure that patents are valid and enforceable.

Finally, study of blockchain technology and the law could also have implications for the way that cybersecurity is protected. This could help to ensure that private information is not accessed or stolen by third parties, and it could also help to improve the understanding of how cybercrime is prevented and investigated.