What is a blockchain and how can it help businesses?

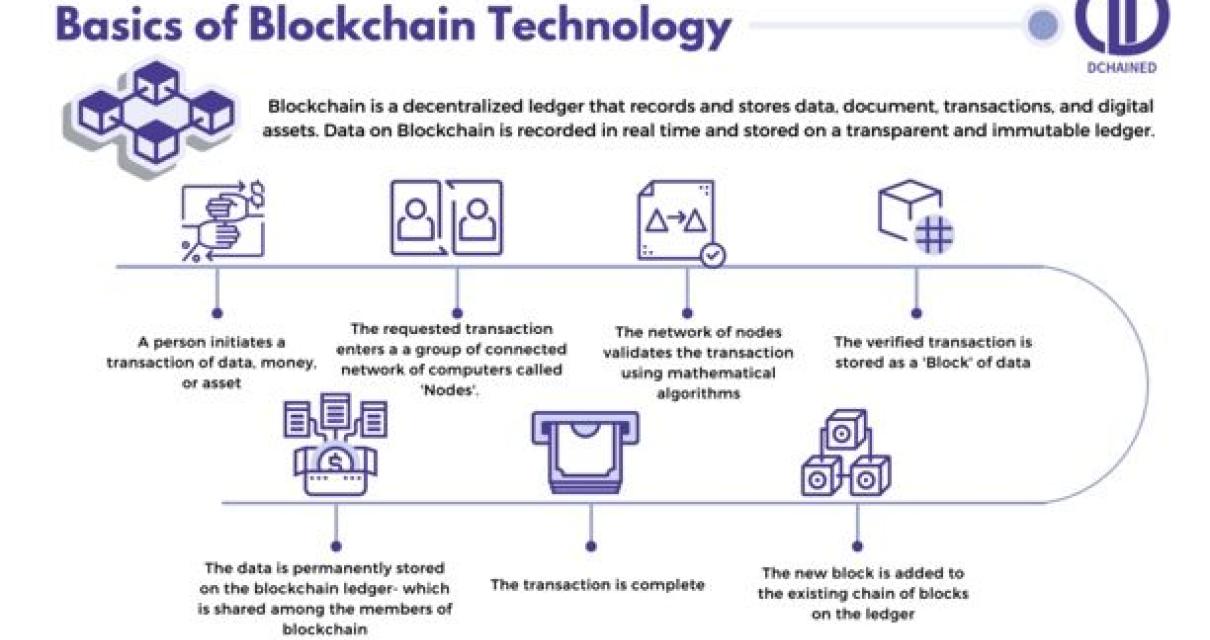

A blockchain is a distributed database that allows for secure, transparent and tamper-proof transactions. It can help businesses by facilitating trust and transparency among participants, reducing the need for third-party verification and eliminating the need for a middleman.

How does a blockchain work?

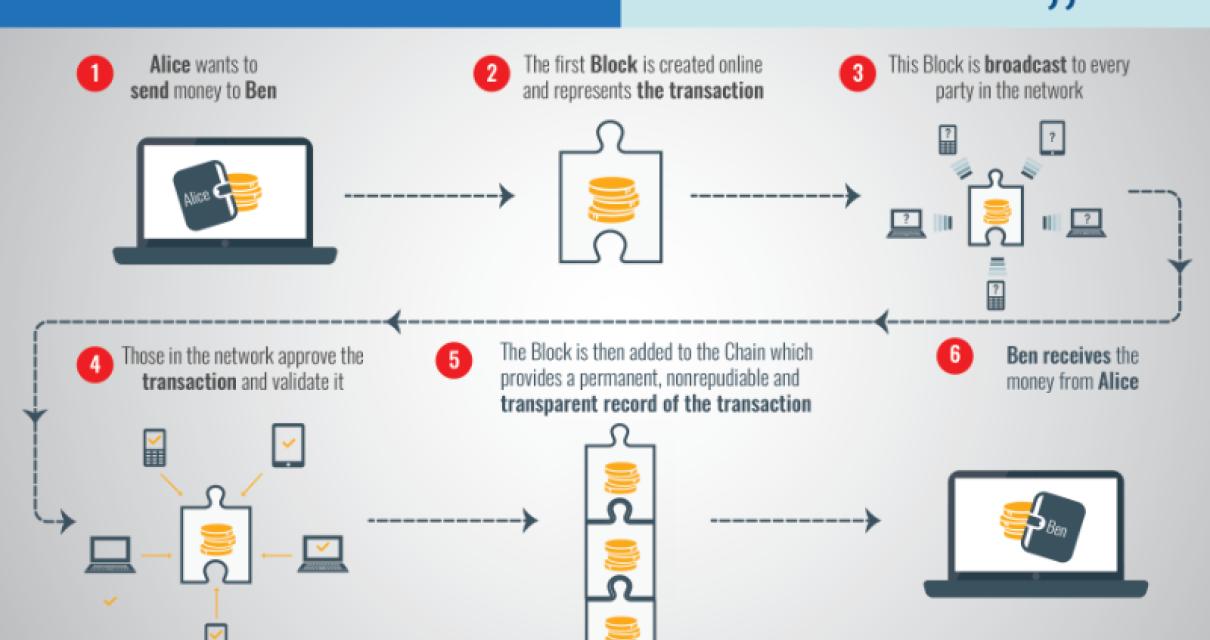

A blockchain is a distributed ledger of all cryptocurrency transactions. It is constantly growing as “completed” blocks are added to it with a new set of recordings. Each block contains a cryptographic hash of the previous block, a timestamp, and transaction data. Bitcoin nodes use the block chain to distinguish legitimate Bitcoin transactions from attempts to re-spend coins that have already been spent elsewhere.

What are the benefits of a blockchain?

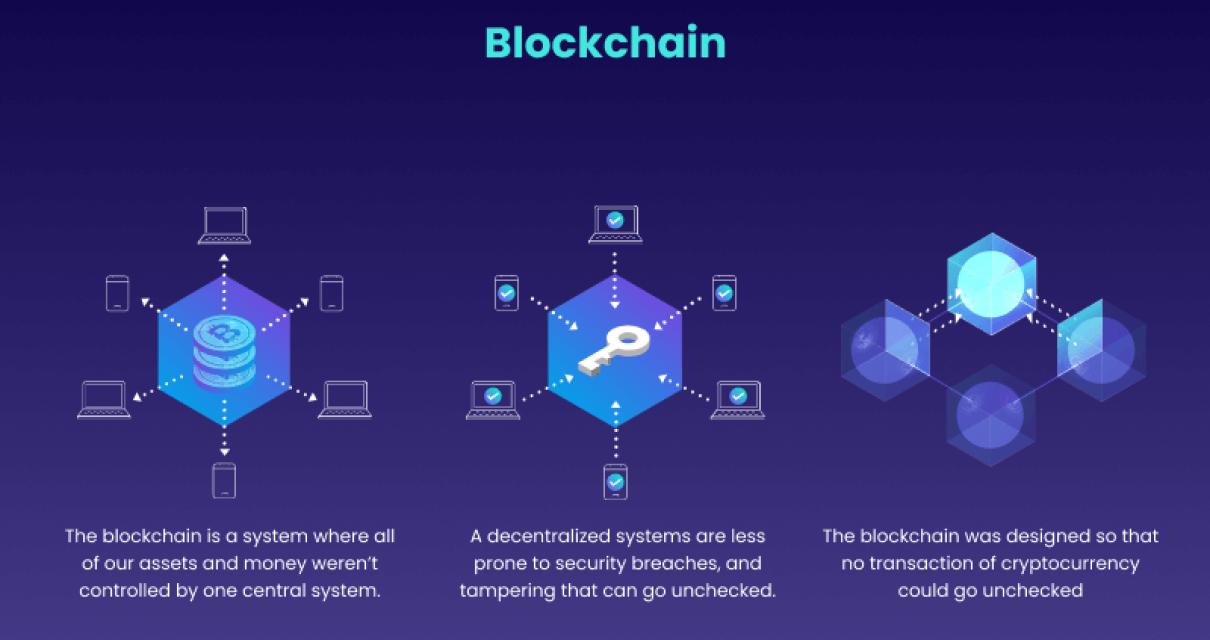

A blockchain is a distributed database that allows for secure, transparent and tamper-proof transactions. Transactions are verified by network nodes and recorded in a public ledger. The benefits of a blockchain include:

1. Transparency: A blockchain is transparent, meaning all the transactions and data stored on it are publicly accessible. This makes it difficult for anyone to tamper with the data or to fraudulently conduct transactions.

2. Security: A blockchain is secure, meaning it is difficult to hack and tamper with the data. The network nodes use cryptography to protect the data.

3. Tamper-proof: A blockchain is tamper-proof, meaning it is impossible for anyone to corrupt or tampering with the data.

4. Cost-effective: A blockchain is cost-effective, meaning it is easier and cheaper to verify and process transactions on a blockchain than on traditional systems.

What are the key features of a blockchain?

A blockchain is a distributed database that enables secure, transparent and tamper-proof transactions. It is a public ledger of all cryptocurrency transactions. The blockchain is constantly growing as “completed” blocks are added to it with a new set of recordings. Each block contains a cryptographic hash of the previous block, a timestamp and transaction data. Bitcoin, Ethereum and other digital currencies are based on blockchain technology.

How can blockchain be used to create trust?

Blockchain can be used to create trust by providing a secure and tamper-proof record of transactions. This record can be used to verify the legitimacy of a transaction and to ensure that all parties involved in a transaction are aware of it.

How can blockchain be used to improve transparency?

One way that blockchain could be used to improve transparency is by allowing users to track the origin and progression of a transaction. This information would be available on a public ledger, allowing for more transparency and accountability in financial systems. Additionally, blockchain could be used to create tamper-proof records of transactions, which would further enhance transparency and accountability.

What are some of the challenges associated with blockchain?

Some of the challenges associated with blockchain include scalability, security, and reliability. Additionally, blockchain technology is still in its early stages and faces many challenges in terms of adoption.

How can businesses make use of blockchain technology?

There are a few ways businesses can make use of blockchain technology. For example, businesses could use blockchain to securely store documents such as contracts and agreements. Additionally, blockchain technology could be used to track the movement of goods across supply chains. Finally, blockchain technology could be used to facilitate payments between businesses.

What impact will blockchain have on business in the future?

There is no one answer to this question as the impact of blockchain on business will vary depending on the specific business and its needs. However, some experts believe that blockchain could have a major impact on how businesses operate by providing a more secure and transparent platform for transactions. Additionally, blockchain could help speed up the process of making transactions and could even help reduce costs associated with transactions.

How is blockchain changing the way we do business?

Bitcoin and blockchain are changing the way we do business by providing a secure and transparent way to conduct transactions. Transactions are verified and recorded on a public ledger, which allows businesses to avoid the risk of fraud and corruption. Additionally, blockchain is creating a new platform for entrepreneurs to create and invest in new businesses.

What are the implications of blockchain for business?

The implications of blockchain for business are largely dependent on the specific use case. For example, if a business is looking to create a tamper-proof record of transactions, blockchain would be a suitable solution. If, however, a business is looking to create a peer-to-peer network for exchanging goods or services, then a different type of blockchain may be more appropriate.

How can businesses benefit from blockchain technology?

There are many ways businesses can benefit from blockchain technology. Some of the ways businesses can benefit are as follows:

1. Blockchain technology can help businesses to reduce costs associated with traditional transactions. For example, blockchain can help to reduce the need for third-party verification and authentication processes, which can save businesses time and money.

2. Blockchain technology can help to secure and verify transactions more effectively than traditional systems. This can help to avoid potential fraud and other issues that can occur with traditional transactions.

3. Blockchain technology can help to create a more transparent system for businesses and consumers. This can help to ensure that all parties involved in a transaction are aware of the details of the deal, which can improve trust between parties.

4. Blockchain technology can help to reduce the overall time it takes to complete a transaction. This can help to speed up the process of completing transactions and improving customer service.