How will blockchain technology affect insurance?

Blockchain technology could have a major impact on the insurance industry by allowing customers to securely and transparently store information about their insurance policies. This would allow insurers to provide more accurate quotes and reduce the amount of time needed to process claims. Additionally, blockchain technology could help to create a tamper-proof record of insurance transactions, which would make it difficult for fraudsters to commit insurance fraud.

The impact of blockchain technology on insurance

There is no doubt that blockchain technology has the potential to revolutionize the insurance industry. By providing a secure and transparent platform for managing risks, blockchain could enable insurers to reduce costs, improve customer experience, and speed up the process of settling claims.

Some of the biggest benefits of blockchain technology for the insurance sector include:

Reduced Costs: Blockchain provides a secure and transparent platform for managing risks, which could reduce insurers’ costs. For example, by automating the settlement process, blockchain could reduce the time it takes to pay out claims, and by reducing the number of intermediaries involved in the process, it could save insurers money on fees.

Improved Customer Experience: Blockchain could also improve customer experience by providing a secure and transparent platform for tracking and tracing assets. This could help customers to understand their insurance policy better and make claims faster.

Speed Up the Process of Settling Claims: By providing a secure and transparent platform for managing risks, blockchain could speed up the process of settling claims. For example, by automating the process of verifying claims and settling payments, blockchain could reduce the time it takes to pay out claims.

How will the insurance industry be affected by blockchain technology?

There is no one definitive answer to this question as the impact of blockchain technology on the insurance industry will vary depending on the specifics of the case. However, some potential impacts of blockchain technology on the insurance industry could include increased transparency and security within the system, increased efficiency and cost-savings, and the potential for new business models.

The potential of blockchain technology in the insurance industry

There are a number of potential applications for blockchain technology in the insurance industry, including tracking and tracing insurance claims, automating the management of insurance policies, and improving transparency and trust in the industry.

Tracking and tracing insurance claims

One potential application for blockchain technology in the insurance industry is tracking and tracing insurance claims. Blockchain technology can help to ensure that insurance claims are processed in a transparent and secure way, and that information about each claim is available to all involved parties.

Automating the management of insurance policies

Another potential application for blockchain technology in the insurance industry is automating the management of insurance policies. Blockchain technology can help to improve the accuracy and timeliness of insurance policy information, and to reduce the need for human input.

Improving transparency and trust in the industry

Blockchain technology can also help to improve transparency and trust in the insurance industry. By making information about insurance claims and policy transactions available on a public blockchain, the industry can become more transparent and accountable. Additionally, blockchain technology can help to create a more secure environment for insurance transactions, by encrypting sensitive data using cryptography.

How blockchain technology could reshape the insurance industry

There are a number of ways in which blockchain technology could reshape the insurance industry. For example, it could help to reduce the cost of insurance premiums, by providing a more efficient and secure system for processing claims. It could also help to improve the transparency of the insurance process, by providing a secure and tamper-proof record of all transactions. Finally, it could help to reduce the risk of fraud and cyber-attacks, by ensuring that all data is securely stored and accessible.

The game-changing potential of blockchain technology for insurance

Blockchain technology is a distributed ledger that allows for secure, transparent and immutable transactions between parties. It has the potential to revolutionize the insurance industry by creating a more efficient and transparent system for managing risk.

One of the key benefits of blockchain technology is that it eliminates the need for a trusted third party. Instead, it allows for peer-to-peer transactions between parties, which is more reliable and secure. This means that insurance companies can avoid the costs and inefficiencies associated with traditional systems.

Additionally, blockchain technology can help to improve transparency and accuracy of insurance claims processing. It can also help to reduce fraud and waste, making the system more efficient and accountable.

Overall, blockchain technology has the potential to revolutionize the insurance industry by creating a more efficient and transparent system for managing risk. It has the potential to reduce costs and improve performance, making the system more customer-friendly and responsive.

How could blockchain technology transform insurance?

Blockchain technology could transform insurance by providing a tamper-proof and secure platform for recording and tracking insurance transactions. This would make it easier for insurers to identify and resolve disputes, and would also make it easier for policyholders to access their insurance policies.

The revolutionary potential of blockchain technology for insurance

The potential of blockchain technology for insurance is enormous. In theory, it could be used to create a more efficient and secure system for managing insurance transactions. It could also help to reduce the cost of insurance premiums.

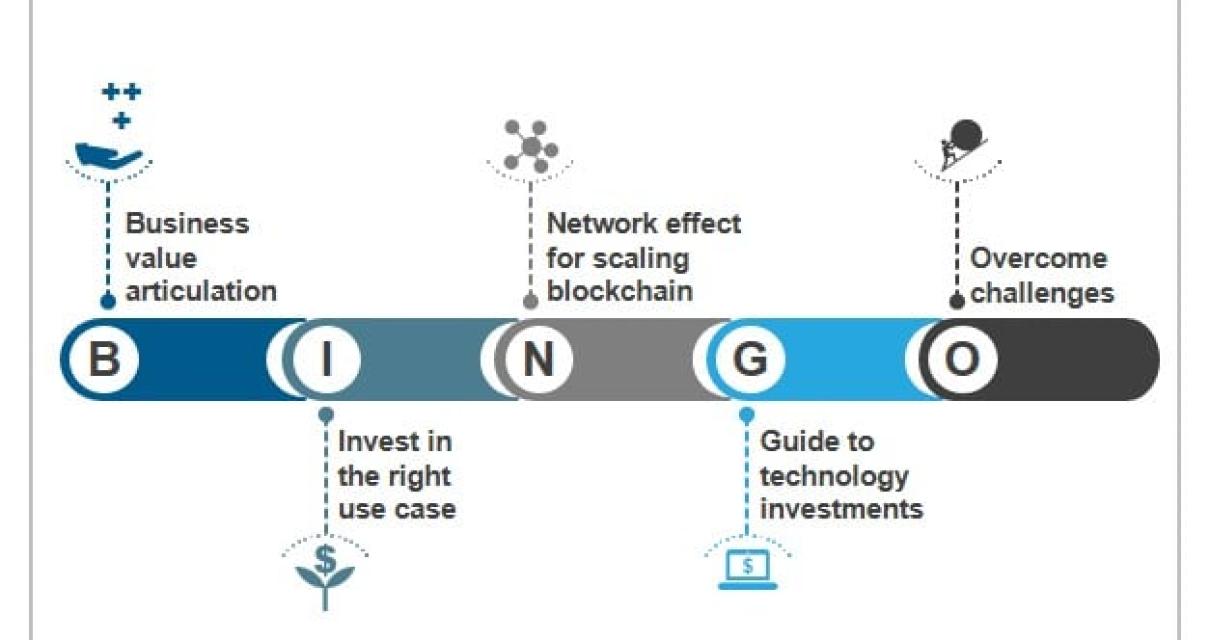

However, there are a number of challenges that must be overcome before blockchain technology can be successfully used in the insurance sector. First, regulators must be convinced of the benefits of using blockchain technology. Second, insurers must be able to understand and adopt the technology. Third, they must find a way to integrate it into their existing systems. Finally, there is the question of how to price insurance products using blockchain technology.

Nevertheless, if all goes well, blockchain could eventually revolutionize the way insurance is conducted.

How will blockchain technology change the insurance landscape?

Blockchain technology is expected to change the insurance landscape in a few ways. First, it could make it easier for customers to access insurance products and services. Second, it could make it easier for insurance companies to collect premiums and make payments. And finally, it could make it easier for insurers to manage risks.

The implications of blockchain technology for insurance

There are a number of potential implications of blockchain technology for insurance, including the following:

1. Increased transparency and security: Blockchain technology can help to increase transparency and security across a variety of insurance transactions, including claims processing and policy issuance. By reducing the amount of time needed to process transactions and issuing policies electronically, blockchain could potentially improve trust between insurers and customers.

2. Reduced costs and improved efficiency: Blockchain technology could also lead to reduced costs and improved efficiency for insurers in a number of areas, including policy issuance and claims processing. By automating these processes, blockchain could save insurers time and money.

3. Improved customer experience: In addition to reducing costs and improving efficiency, blockchain technology could also improve customer experience by providing a more transparent and secure system for making transactions. By eliminating the need for third-party intermediaries, blockchain could potentially reduce the amount of time needed to process claims and policy applications.

4. Greater flexibility and scalability: Another potential benefit of blockchain technology is its flexibility and scalability. By allowing for the tracking and recording of transactions across a large number of participants, blockchain could potentially enable insurers to scale up their operations without sacrificing quality or accuracy.

What does the future hold for blockchain technology and insurance?

Blockchain technology is expected to continue to grow in popularity and be used in a variety of industries, including insurance. The technology could help streamline the process of exchanging information and payments between insurers and customers, and it could also help insurers manage their risks more efficiently.