Introduction to blockchain technology

Blockchain technology is a distributed database that allows for secure, transparent and tamper-proof transactions. Transactions are verified by network nodes through cryptography and recorded in a public ledger. Bitcoin, the first and most well-known blockchain application, uses a peer-to-peer network to operate with no central authority.

The potential benefits of blockchain technology include:

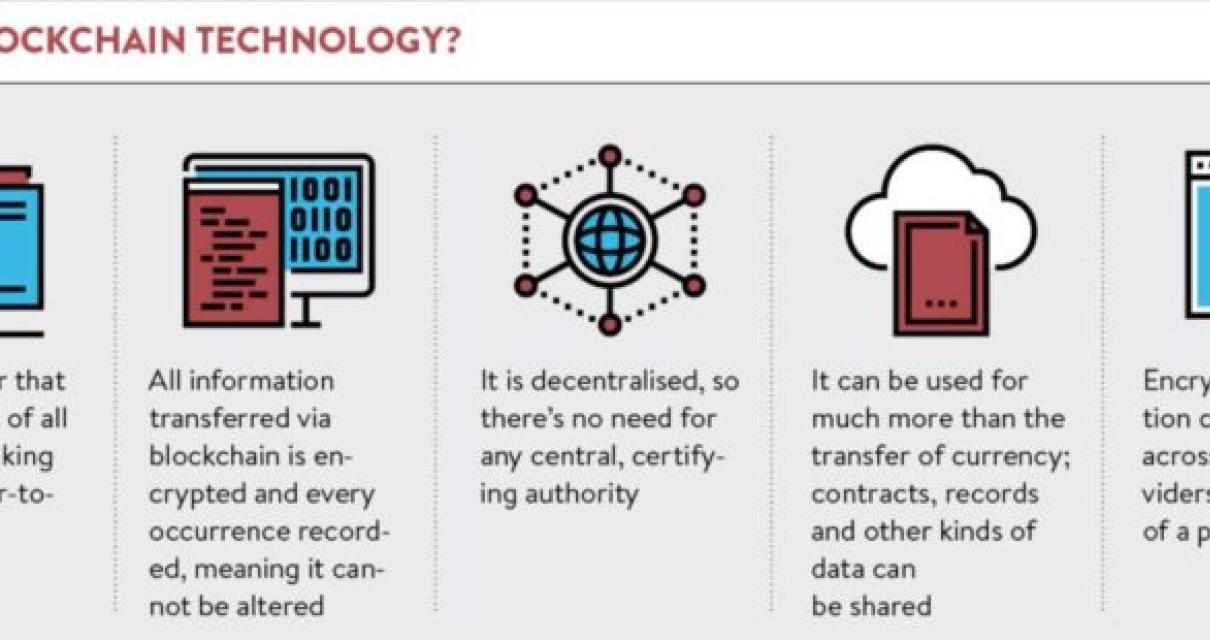

Security: Transactions are verified by network nodes through cryptography and recorded in a public ledger. This makes it difficult for attackers to counterfeit or fraudulentate transactions.

Transparency: Every participant on the blockchain network can see every transaction that has ever been made. This transparency makes it easy to track who owns what and eliminates the need for third-party intermediaries.

Tamper-proof: Transactions on the blockchain are immune to modification or deletion once they have been recorded. This makes it difficult for attackers to corrupt the system or steal data.

Although blockchain technology has a number of potential benefits, there are also some potential risks associated with it. For example, blockchain technology is not without its own set of vulnerabilities. In addition, not all Network nodes will accept a blockchain transaction, which could lead to delays in processing transactions.

What is blockchain technology?

Blockchain technology is a distributed database that maintains a continuously growing list of records called blocks. Each block contains a cryptographic hash of the previous block, a timestamp, and transaction data. Bitcoin and other cryptocurrencies use blockchain technology to maintain a public ledger of all transactions.

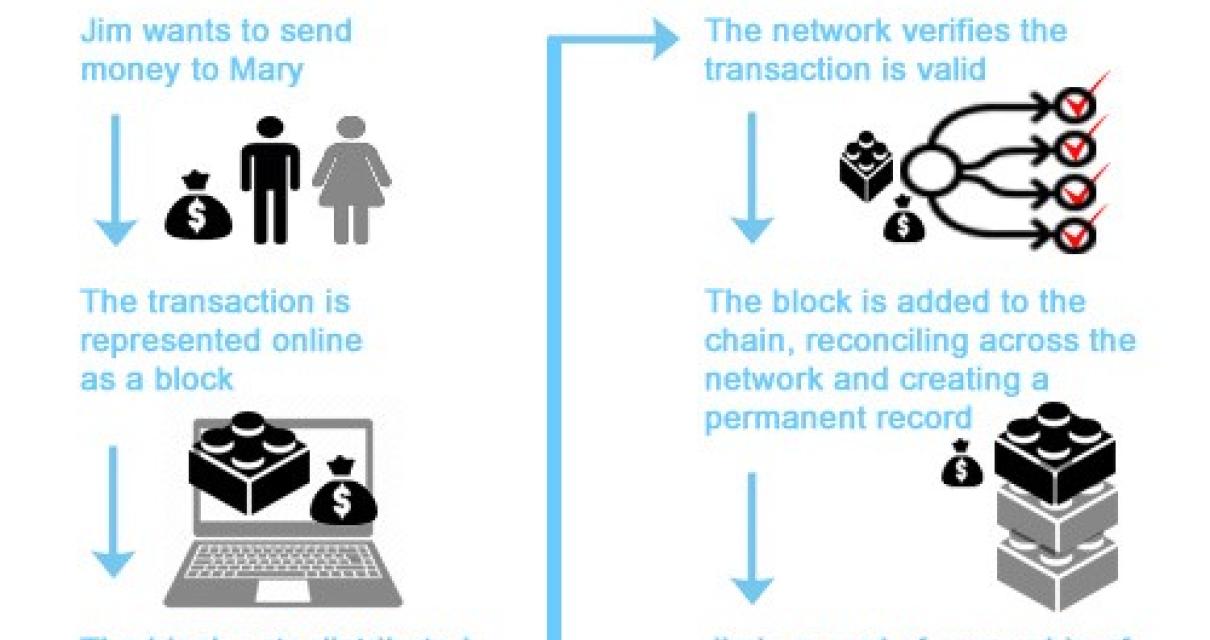

How does blockchain technology work?

Blockchain technology is a distributed database that allows for secure, transparent and tamper-proof transactions. Transactions are verified by network nodes and recorded in a public distributed ledger called a blockchain. Bitcoin, first proposed by Satoshi Nakamoto, was the first decentralized digital currency.

The benefits of blockchain technology

There are many potential benefits of blockchain technology, including:

1. transparency: All transactions on a blockchain are publicly visible and transparent, making it an efficient way to track and monitor transactions.

2. security: Blockchain technology is secure because it uses a distributed database that is protected by cryptography.

3. trust: Blockchain technology can help build trust between parties because transactions are verified by network nodes and recorded in a public ledger.

4. scalability: Blockchain technology can handle large volumes of transactions without slowing down.

5. cost-efficiency: Blockchain technology is cost-effective because it eliminates the need for third-party intermediaries.

The potential of blockchain technology

There are a number of potential applications for blockchain technology, including:

-Distributed ledgers could be used to track the ownership of assets and facilitate transactions.

-Blockchain could be used to create a tamper-proof record of transactions.

-It could be used to create a secure system for exchanging money or assets.

-It could be used to create a digital marketplace for goods and services.

The challenges of blockchain technology

The key benefits of blockchain technology are its transparency, security, and immutability. However, these benefits come with a number of challenges.

Transparency: Blockchain technology is transparent, meaning that everyone can see the transactions taking place on the network. This transparency makes it difficult for criminals to operate undetected, as they would need to know the details of the transactions taking place.

Security: Blockchain technology is secure, meaning that it is difficult for hackers to access and steal information. The security of blockchain technology is based on the fact that it is decentralized, meaning that there is no central authority that can be hacked.

Immutability: blockchain technology is immutable, meaning that the records of transactions cannot be changed. This is a key benefit of blockchain technology, as it ensures that information is accurate and secure.

The future of blockchain technology

The future of blockchain technology is bright. It has the potential to revolutionize many industries, including financial services, supply chain management, and healthcare.

The technology has the potential to reduce costs and improve transparency across a variety of industries. It could also reduce the risk of fraud and corruption.

Overall, blockchain technology is continuing to grow in popularity and has the potential to revolutionize many industries.

What is a distributed ledger?

A distributed ledger is a digital ledger of transactions that is shared by many participants. Transactions are verified and recorded in a chronological order, and all participants can access the ledger to verify its accuracy. This makes it an ideal platform for managing transactions and tracking assets.

What are smart contracts?

Smart contracts are self-executing contracts that run on a blockchain. They allow two or more parties to make a contract without the need for a third party. The contract is automatically executed when the conditions are met.

What are the use cases of blockchain technology?

There are a number of potential use cases for blockchain technology, including:

-Distributed ledgers can be used to record transactions between parties in a secure and transparent way. This could be used for things like a registry of property rights or a shared database of events.

-Blockchain technology can be used to create tamper-proof records of transactions. This could be used for things like tracking the movement of goods or verifying the legitimacy of a transaction.

-Blockchain technology can be used to create decentralized applications (dApps). These could be used for things like issuing and trading cryptocurrencies, managing file storage, or creating a peer-to-peer marketplace.

-Blockchain technology can be used to create an online marketplace for goods and services. This could be used for things like selling products or services online, or renting out space.

How can blockchain technology be implemented?

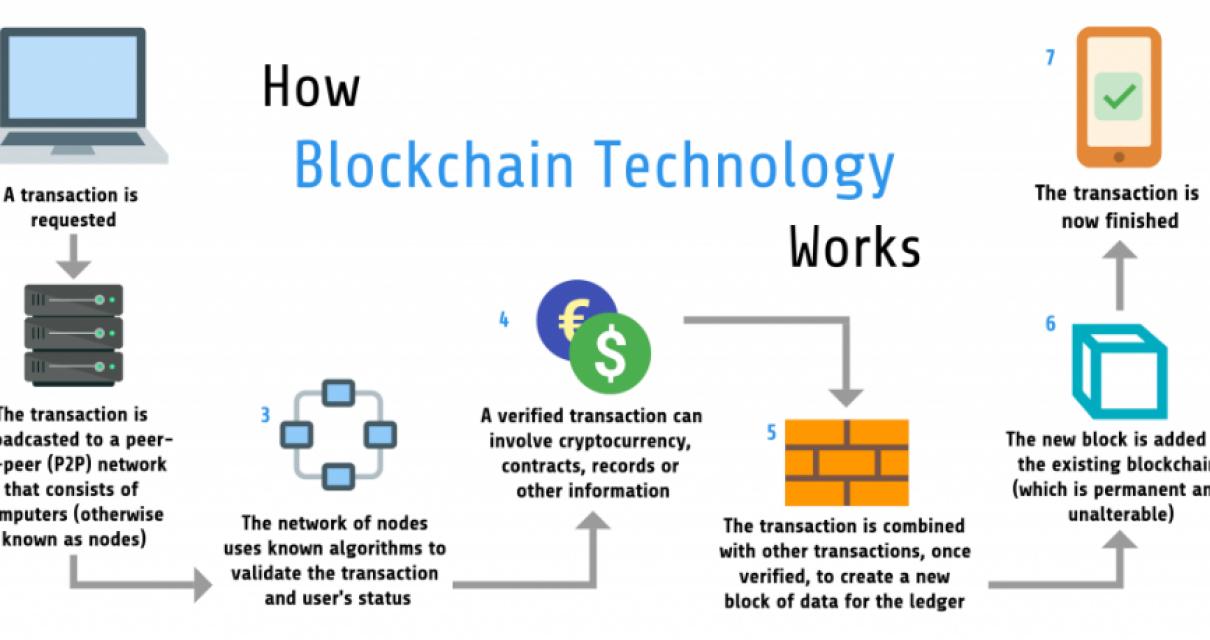

Blockchain technology can be implemented in many ways. A blockchain is a digital ledger of all cryptocurrency transactions. This ledger is decentralized, meaning it is not controlled by one party. Transactions are recorded and verified by network nodes through cryptography and recorded in a chronological order. Nodes can verify transactions, add them to the ledger, and then broadcast these additions to other nodes. Bitcoin and other cryptocurrencies are built on a blockchain.