What is Blockchain?

A blockchain is a decentralized, digital ledger of all cryptocurrency transactions. It is constantly growing as "completed" blocks are added to it with a new set of recordings. Each block contains a cryptographic hash of the previous block, a timestamp, and transaction data. Bitcoin nodes use the block chain to differentiate legitimate Bitcoin transactions from attempts to re-spend coins that have already been spent elsewhere.

How does Blockchain work?

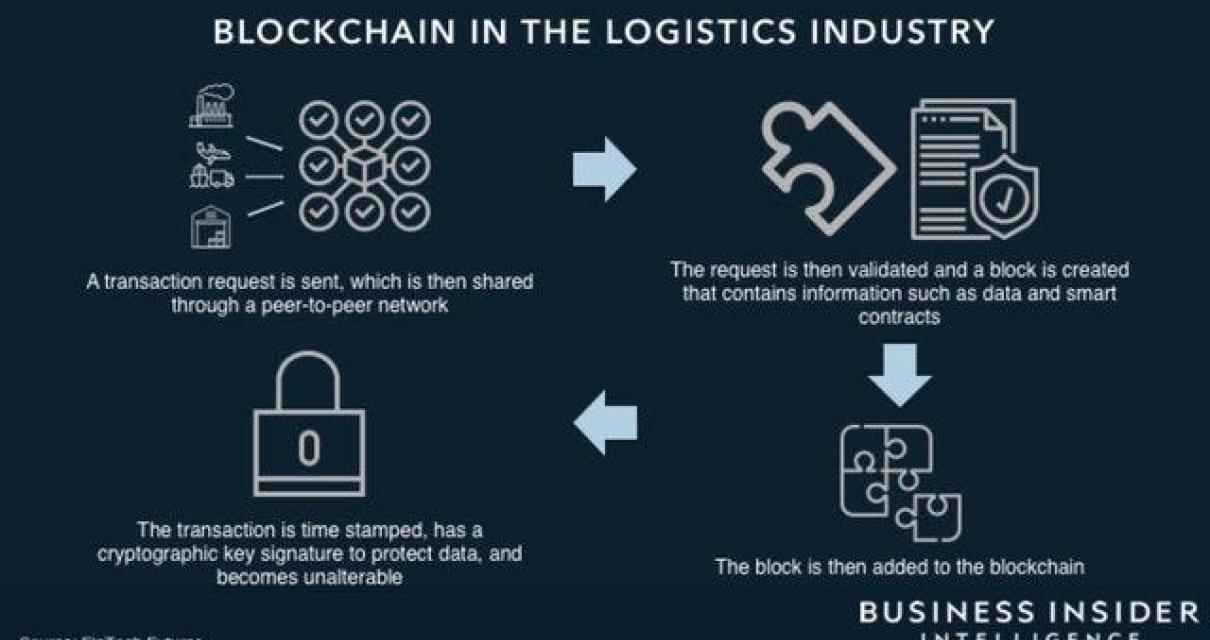

Blockchain is built on a peer-to-peer network. Each node computers on the network maintains a copy of the blockchain. Whenever a new block is added to the blockchain, every node on the network updates its copy of the blockchain. Nodes that don't have a copy of the blockchain (or don't want to update their copy) can ignore the new block.

How many nodes are on the Bitcoin network?

There are currently 10,000 nodes on the Bitcoin network.

What is a Blockchain Ledger?

A blockchain ledger is a digital ledger of all cryptocurrency transactions. It is constantly growing as "completed" blocks are added to it with a new set of recordings. Each block contains a cryptographic hash of the previous block, a timestamp, and transaction data. Bitcoin nodes use the block chain to differentiate legitimate Bitcoin transactions from attempts to re-spend coins that have already been spent elsewhere.

How Does Blockchain Work?

A blockchain is a distributed database that can be used to track the ownership of digital assets. Transactions are verified and recorded in a chronological order using cryptography. Each node in the network has a copy of the blockchain, and every transaction that takes place is verified by the network. Bitcoin, Ethereum, and other cryptocurrencies are all based on a blockchain.

Benefits of Blockchain Technology

1. Reduced Costs and Time to Market

Blockchain technology reduces the costs and time needed to develop, deploy and manage a business or product. It also allows for secure, transparent and automated transactions.

2. Increased Security and Transparency

The distributed ledger technology used in blockchain is highly secure and transparent. Transactions are verified and recorded in a public ledger, which makes it difficult for hackers to tamper with data.

3. Reduced Intermediation and Increased Efficiency

The decentralized nature of blockchain technology allows for increased efficiency and reduction of intermediaries between buyers and sellers. This lowers the costs of transactions and improves trust and security.

4. Greater Accountability and Transparency

With blockchain technology, companies can ensure greater accountability and transparency for their operations. This can help to improve trust and confidence among customers and stakeholders.

Uses of Blockchain Technology

There are many potential uses for blockchain technology, but some of the most common include:

1. Recording and storing transactions on a tamper-proof public ledger.

2. Tampering with transactions or data on the blockchain is difficult because all the copies of the ledger are constantly updated.

3. Cryptocurrencies such as Bitcoin and Ethereum are built on blockchain technology.

4. Companies can use blockchain technology to create a secure and transparent online transaction system.

5. The technology can be used to track the ownership of assets such as intellectual property or land titles.

Blockchain Technology: Pros and Cons

There are many pros to using blockchain technology, but there are also some cons that should be considered before implementing it in a business.

Pros of Blockchain Technology:

1. Immutability: Blockchain is an immutable technology, meaning that all data is stored on a public ledger and cannot be changed. This makes it an ideal solution for businesses that need to keep track of transactions and information.

2. Security: Blockchain is secure because it is decentralized and uses a cryptographic algorithm to protect data. This makes it difficult for hackers to gain access to data and disrupt the system.

3. Transparency: All transactions on a blockchain are transparent, which allows businesses to see how much money they are spending and how much money they are making. This is an important feature for businesses that need to be transparent with their customers and investors.

4. Low Costs: Blockchain technology is relatively low cost, which makes it an ideal solution for small and medium businesses (SMBs).

5. Fast Transactions: Transactions on a blockchain are fast, which makes it an ideal solution for businesses that need to make quick decisions.

Cons of Blockchain Technology:

1. Volatility: Blockchain technology is volatile, which means that the value of a cryptocurrency can change rapidly. This is an issue for businesses that need to plan for long-term investments.

2. Lack of Scalability: Blockchain technology is not scalable, which means that it cannot handle large numbers of transactions. This could be a problem for businesses that need to process a lot of transactions quickly.

3. High Fees: Blockchain technology has high fees, which makes it difficult for businesses to use it for transactions. This could be a problem for businesses that need to process a lot of transactions quickly.

4. Inability to Handle Large Amounts of Data: Blockchain technology is not able to handle large amounts of data, which could be a problem for businesses that need to store a lot of information on the blockchain.

5. Limited Use Cases: Blockchain technology has limited use cases, which means that it is not suitable for all businesses. This could be a problem for businesses that want to use blockchain technology but do not know where to start.

Is Blockchain the Future of Ledger Technologies?

Blockchain technology has the potential to revolutionize how we do business and manage our finances. It offers a secure, tamper-proof record of transactions that can be verified by anyone. This could lead to significant improvements in efficiency and transparency across a wide range of industries. However, there is still some way to go before blockchain is widely adopted.