How businesses are using blockchain to streamline operations

The use of blockchain technology by businesses has a number of potential applications, including reducing costs, improving customer experience and speeding up transactions. Here are a few examples:

1. Supply chain management: Blockchain can be used to improve the flow of goods throughout a supply chain, from the manufacturer to the retailer. By tracking the origin and journey of each item, businesses can eliminate duplicate or fraudulent transactions, and improve accuracy and transparency of information.

2. Loyalty programs: Loyalty programs can be implemented using blockchain technology to create a more efficient and secure system. The program could track all rewards points, including those earned through digital or physical cards, and automatically send out rewards to customers when they reach predefined milestones. This would reduce the need for customer service staff, and significantly reduce the processing time and associated costs.

3. Records management: Businesses can use blockchain to manage records securely and transparently. The technology can be used to create a tamper-proof record of all transactions, which can be accessed by authorized personnel only. This could help to reduce fraud and protect intellectual property rights.

4. Cross-border payments: Blockchain can be used to make international payments faster and more secure. By creating a distributed ledger of transactions, businesses can avoid the fees charged by traditional banks and payment processors.

5. Supply chain management: Blockchain can also be used to improve the flow of goods throughout a supply chain, from the manufacturer to the retailer. By tracking the origin and journey of each item, businesses can eliminate duplicate or fraudulent transactions, and improve accuracy and transparency of information.

How blockchain is improving business transparency

Blockchain technology is improving business transparency by making it easier for companies to share information with each other and with their customers. For example, a company can use blockchain to track the origin of a product, the steps it took to produce it, and the identities of the people who made it. This information can help customers make more informed decisions about their purchases and protect them from unwanted interactions with dishonest businesses.

How blockchain is being used to fight business fraud

Blockchain technology is being used in a variety of ways to fight business fraud. One example is using blockchain to track the ownership of assets. This can help prevent fraudsters from stealing assets or using them for other purposes. It can also help businesses track the origins of assets. This can help prevent fraudsters from falsely claiming assets as their own. In some cases, blockchain can also be used to create a tamper-proof record of transactions. This can help prevent fraudsters from altering or falsifying records.

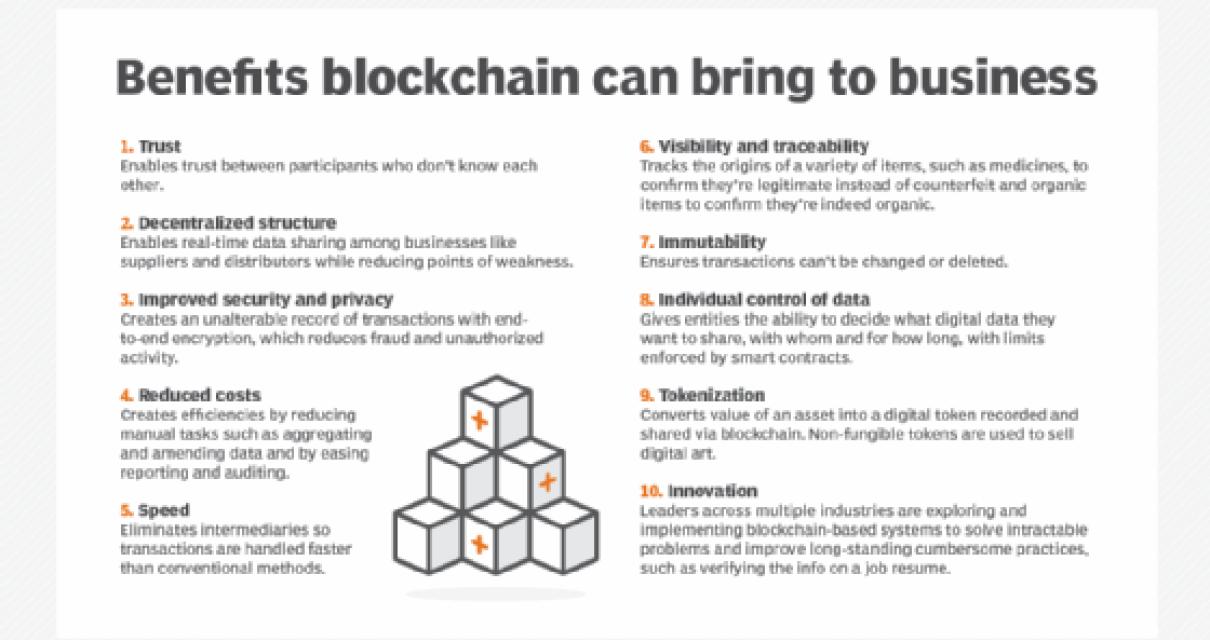

The benefits of blockchain for businesses

There are a number of potential benefits to using blockchain technology for businesses. These include:

1. Increased security and transparency: Blockchain technology can help to increase security and transparency by ensuring that all transactions are recorded and accessible by all participants. This can help to prevent fraudulent activities, and ensure that all relevant information is available to stakeholders.

2. Reduced costs and improved efficiency: Blockchain technology can help to reduce costs and improve efficiency by cutting out the need for third-party intermediaries. This can help to reduce the time and cost involved in executing transactions, and make it easier to track and manage finances.

3. Increased trust and credibility: Blockchain technology can help to build trust and credibility by ensuring that all participants are aware of all transactions taking place, and that these transactions are verified by a network of trusted nodes. This can help to reduce the risk of fraud and corruption, and increase the faith that users have in the system.

4. Increased transparency and accountability: Blockchain technology can help to increase transparency and accountability by providing a secure and tamper-proof record of all transactions. This can help to ensure that companies are held accountable for their actions, and that customers can easily access information about the company’s operations.

The potential of blockchain for businesses

There are a number of potential benefits that could be realized by businesses when it comes to blockchain. These include:

Reduced costs: Blockchain can help to reduce the costs associated with transactions, such as the need for a third party to facilitate the process. This could lead to significant savings for businesses.

Reduced timeframes: Transactions can be completed more quickly and easily through the use of blockchain technology, which could lead to improved efficiency.

Increased security: Blockchain technology can help to ensure that data is secure and tamper-proof, making it a more reliable means of storing information.

Improved transparency: With blockchain, businesses can ensure that all relevant information is available in a publicly accessible format, which could lead to increased transparency and accountability.

Improved customer experience: With blockchain technology, customers can access information more quickly and easily, which could lead to improved customer satisfaction.

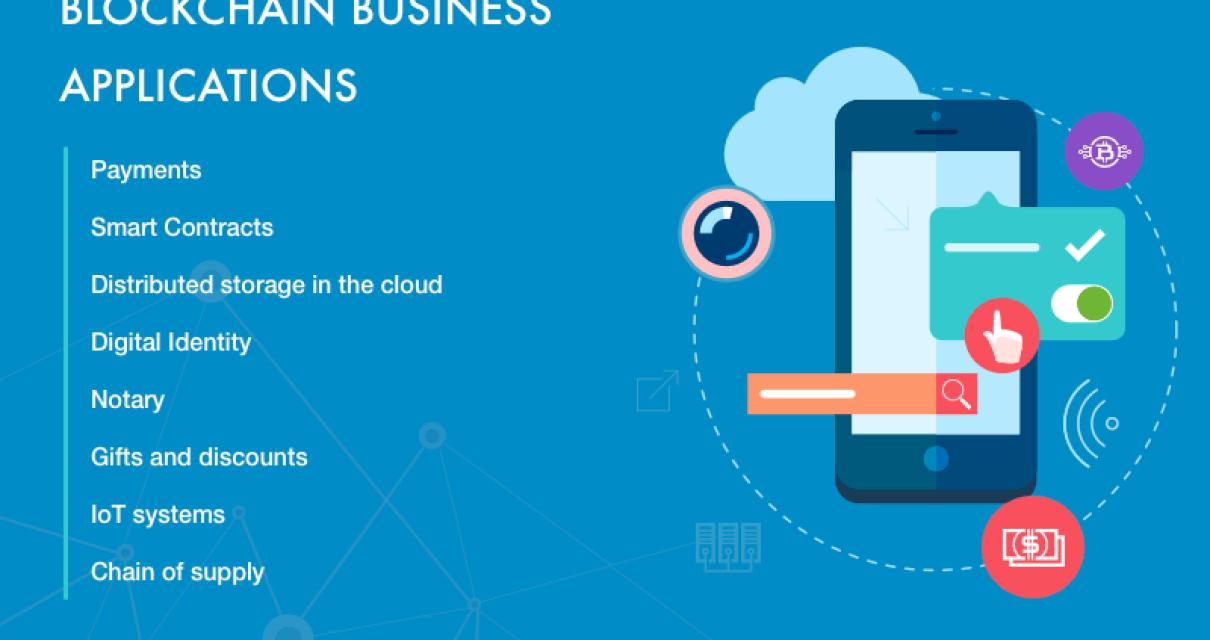

How businesses can make use of blockchain

There is no one definitive answer to this question, as the use of blockchain technology by businesses varies greatly. However, some possible uses for blockchain technology in businesses include:

1. Tampering-proof ledgers: A blockchain can be used to create a tamper-proof ledger of all transactions that take place on the network. This can be used to ensure that transactions are accurate and reliable, and that no one party can manipulate the data.

2. Secure data storage: A blockchain can be used to securely store data in a decentralized manner. This protects the data from being tampered with or stolen, and it makes it difficult for third parties to access the data.

3. Safe and transparent transactions: A blockchain can be used to provide a safe and transparent way for businesses to conduct transactions. This minimizes the chances of fraud or other malicious activities taking place, and it ensures that all parties involved in the transaction are aware of the details of the deal.

4. Improved transparency and trust: A blockchain can help to improve the transparency and trustworthiness of business transactions. This ensures that all parties involved in the deal are aware of the details of the deal, and that there is no chance of fraud or other malicious activities taking place.

What challenges does blockchain pose for businesses?

There are a few key challenges that businesses face when it comes to blockchain. One challenge is that blockchain technology is still relatively new, and there is still a lot of development needed in order for it to be adopted by businesses. Another challenge is that blockchain is not yet widely accepted, and some people may not be familiar with it. Finally, businesses need to be aware of the potential security risks associated with using blockchain technology, as there is always the potential for cyberattacks.

Is blockchain really beneficial for businesses?

There is no one-size-fits-all answer to this question, as the benefits of blockchain for businesses will vary depending on the specific business and its needs. However, some potential benefits of using blockchain in business include:

Reduced costs: Blockchain can help reduce the costs associated with processing and recording transactions, such as fees associated with traditional banking systems.

Fraud prevention: Because blockchain is a distributed ledger, it can help prevent fraud by tracking the movement of assets and records across multiple institutions.

Increased transparency: Blockchain can help increase transparency by providing a secure and permanent record of transactions. This can help ensure that all parties involved in a transaction are aware of its details, which can reduce the chances of fraud or other irregularities.

Improved data security: Because blockchain is decentralized, it can help protect data from being tampered with or stolen. Additionally, because the data is stored on a publicly accessible ledger, it can be easier for businesses to verify the accuracy of data.

Reduced risk: By using blockchain, businesses can reduce the risk of fraud or other cyber-attacks by making it more difficult for criminals to tamper with records. Additionally, by using blockchain technology, businesses can eliminate the need for third-party verification of transactions, which can lower the risk of fraud.

Why some businesses are hesitant to adopt blockchain

There are a few reasons why businesses may be hesitant to adopt blockchain technology. First, blockchain is still in its early stages, and there is a lot of uncertainty about how it will develop. Second, blockchain is a complicated technology, and it may be difficult for businesses to understand and implement it. Finally, there is the risk that blockchain technology might not be viable or profitable, and businesses may not be able to overcome these challenges.

How can businesses make the most out of blockchain?

There are many ways businesses can make the most out of blockchain. One way is to use it to create a more secure system for managing transactions. Another way is to use it to create a more efficient system for tracking and storing information.

What the future holds for blockchain and business

There is no one answer to this question, as the future of blockchain and business is still emerging and largely unknown. However, some experts believe that blockchain technology has the potential to revolutionize a number of industries, including finance, shipping, and insurance. In the short term, it is likely that we will see more development and experimentation around blockchain technology in these areas, as businesses try to understand its potential and find ways to apply it to their own operations.

In the long term, however, it is likely that we will see more widespread adoption of blockchain technology across a wider range of industries. This will likely be driven by the fact that blockchain is a highly secure and transparent platform, which can provide a number of benefits for businesses in terms of efficiency and transparency. As such, there is a good chance that we will see a wave of innovation and implementation in this area over the next few years.