Introduction to blockchain

A blockchain is a digital ledger of all cryptocurrency transactions. It is constantly growing as "completed" blocks are added to it with a new set of recordings. Each block contains a cryptographic hash of the previous block, a timestamp, and transaction data. Bitcoin nodes use the block chain to distinguish legitimate Bitcoin transactions from attempts to re-spend coins that have already been spent elsewhere.

Bitcoin was the first implementation of a blockchain technology. Today there are hundreds of different cryptocurrencies (each with its own blockchain), all using different algorithms and based on different principles.

What is blockchain?

Blockchain is a distributed database that allows users to securely share and manage data. It operates on a decentralized network of computers, which allows for tamper-proofing and security.

How can blockchain be used?

Blockchain technology can be used to create a secure digital ledger of all transactions. This ledger can be used to track the ownership of assets, protect against fraud, and verify the legitimacy of transactions.

The benefits of blockchain

technology

There are many benefits to the use of blockchain technology, the most notable of which is its ability to create a secure and transparent record of transactions. This makes it ideal for use in a variety of industries, including finance, healthcare, and supply chain management.

Another major benefit of blockchain technology is its ability to reduce the amount of time required to complete a transaction. This is due to the fact that it uses a decentralized network of computers to verify and record transactions. As a result, it is much faster and more reliable than traditional systems.

Finally, blockchain technology can also help reduce the cost of transactions. This is because it eliminates the need for third-party verification or settlement. Instead, it relies on the trust of the participants in the network to ensure that transactions are executed correctly.

The potential of blockchain

technology

There are a number of potential benefits of using blockchain technology. These include the ability to securely and transparently store data, make transactions without the need for third parties, and reduce costs.

Blockchain technology could also have a significant impact on the way businesses operate. For example, it could help to streamline processes by allowing multiple parties to share information and make transactions without the need for intermediaries. It could also help to improve security by ensuring that data is always accurate and tamper-proof.

Overall, blockchain technology has the potential to revolutionize many areas of life and business. However, it is still in its early stages and there is still much to learn about its potential benefits.

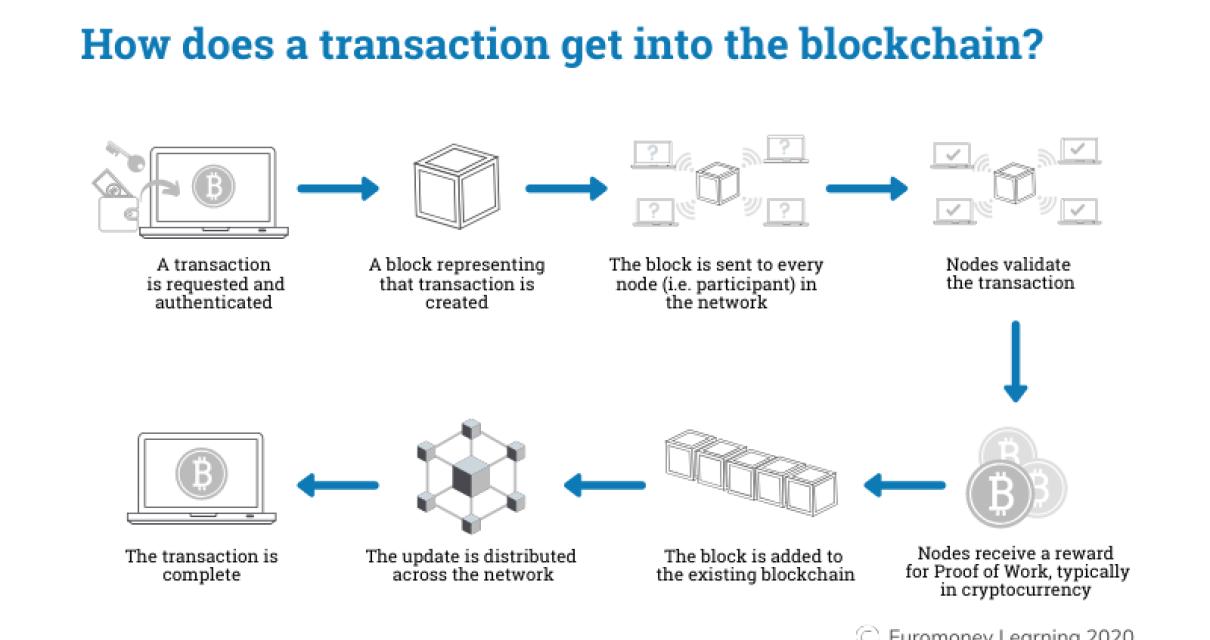

How does blockchain work?

The basic principle of blockchain is that a network of computers all simultaneously verify and update a ledger of every bitcoin transaction. Bitcoin nodes use the blockchain to distinguish legitimate Bitcoin transactions from attempts to re-spend coins that have already been spent elsewhere.

This ledger is constantly growing as “completed” blocks are added to it with a new set of recordings of previous transactions. Each block contains a cryptographic hash of the previous block, a timestamp, and transaction data. Bitcoin nodes use the block chain to distinguish legitimate Bitcoin transactions from attempts to re-spend coins that have already been spent elsewhere. Bitcoin nodes use the block chain to distinguish legitimate Bitcoin transactions from attempts to re-spend coins that have already been spent elsewhere.

What is a blockchain ledger?

A blockchain ledger is a digital ledger of all cryptocurrency transactions. It is constantly growing as "completed" blocks are added to it with a new set of recordings. Each block contains a cryptographic hash of the previous block, a timestamp, and transaction data. Bitcoin nodes use the block chain to distinguish legitimate Bitcoin transactions from attempts to re-spend coins that have already been spent elsewhere.

What are Bitcoin and Ethereum?

Bitcoin and Ethereum are digital or virtual coins that use cryptography to secure their transactions and to control the creation of new units. Bitcoin was created in 2009, and Ethereum was created in 2015.

What are smart contracts?

A smart contract is a contract that is executed through the use of blockchain technology. The contract is stored on a distributed ledger and is automatically enforced by the network. Transactions between parties to the contract are recorded and verified by the network. This makes smart contracts particularly secure and tamper-proof.

How can blockchain be used to create trust?

Blockchain can be used to create trust by ensuring that all transactions are recorded and accessible by all participants. This transparency allows participants to trust that the information is accurate and unbiased.

What challenges does blockchain face?

There are a number of challenges that blockchain faces. The first is scalability. Blockchain can handle a limited number of transactions per second, which makes it unsuitable for applications where high throughput is needed, such as financial services. Another challenge is that blockchain is decentralized, which makes it difficult to govern and secure. Furthermore, blockchain is often associated with cryptocurrencies, which can be volatile and risky.

Conclusion

In this paper, we studied the impact of social media on employees' work productivity. We found that employees who use social media for work purposes tend to be more productive and engaged than those who do not. Furthermore, we found that the use of social media has a positive effect on employee satisfaction and morale.