How to create smart contracts in blockchain

To create a smart contract on the blockchain, you first need to create a digital wallet for your project. Next, you will need to create a contract code. Finally, you will need to deploy the contract to the blockchain.

The benefits of creating smart contracts in blockchain

Smart contracts offer many benefits that make them attractive for use in blockchain applications. These benefits include:

1. Automation: Smart contracts can be automated, which makes them easy to use and reduce the need for human intervention.

2. Transparency: Smart contracts are transparent, which means everyone can see what is being agreed upon and can trust that the terms of the contract will be followed.

3. Security: Smart contracts are secure, meaning that they are protected against attack and cannot be tampered with.

4. Decentralization: Smart contracts are decentralized, meaning they are not subject to the control of any one party. This makes them resistant to censorship and fraud.

5. Accountability: Smart contracts are accountable, meaning that every action taken within them is traceable and can be reviewed. This makes them a reliable way to execute transactions.

The risks of creating smart contracts in blockchain

There are a few risks associated with creating smart contracts in blockchain. The first is that a smart contract can be tampered with, meaning that it can be changed or deleted without anyone noticing. This could lead to serious consequences, such as loss of money or the destruction of valuable data.

Another risk is that a smart contract may not be executed as intended. This could happen for a variety of reasons, including if the code is not properly written or if there is a bug in the software. If this happens, the contract could be invalid and would not be able to execute as intended. This could lead to financial losses for the people involved in the contract, as well as disruption for the wider blockchain network.

Finally, it is important to note that smart contracts are not immune to cyberattacks. If someone is able to breach the security of a smart contract and steal any money or digital assets that are inside it, they could potentially make a lot of money.

The difference between smart contracts and traditional contracts

is that smart contracts are digital contracts that are executed by computers. They are based on blockchain technology, which allows them to be automatically verified and trustless.

How to create a smart contract in blockchain step by step

1. Choose your blockchain platform

There are a variety of different blockchain platforms available, each with its own features and advantages. You can choose whichever blockchain platform is most appropriate for the task at hand.

2. Create a wallet

Before you can start building your smart contract, you need to create a wallet on the chosen blockchain platform. A wallet is a personal account where you can store your private keys. These keys are necessary for making transactions on the platform, as well as for interacting with your smart contracts.

3. Create a custom token

Next, you need to create a custom token. A custom token is a digital asset that represents something else. In this case, you will be creating a token that represents a share in a future project.

4. Create a template smart contract

Next, you need to create a template smart contract. This template will serve as a model for your own smart contract. You will need to customize it to reflect the specific requirements of your project.

5. Add your custom token details

Now, you need to add the details of your custom token. This includes the name of the token, the total number of tokens issued, and the price at which the tokens will be sold.

6. Add your contract details

Next, you need to add the details of your contract. This includes the address of your contract, the rules governing how it works, and the conditions under which it can be executed.

7. Add your user interface details

Finally, you need to add the details of your user interface. This includes the details of how users will be able to access and use your contract.

What you need to know before creating a smart contract in blockchain

Before you create a smart contract in blockchain, it's important to understand what they are and what they can do.

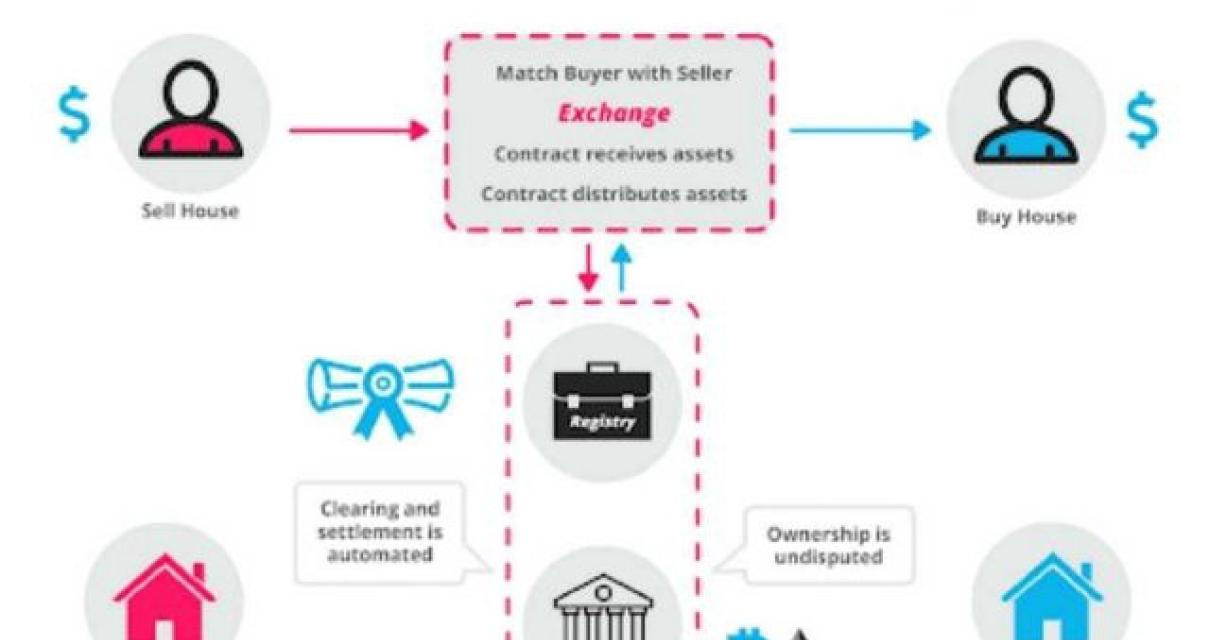

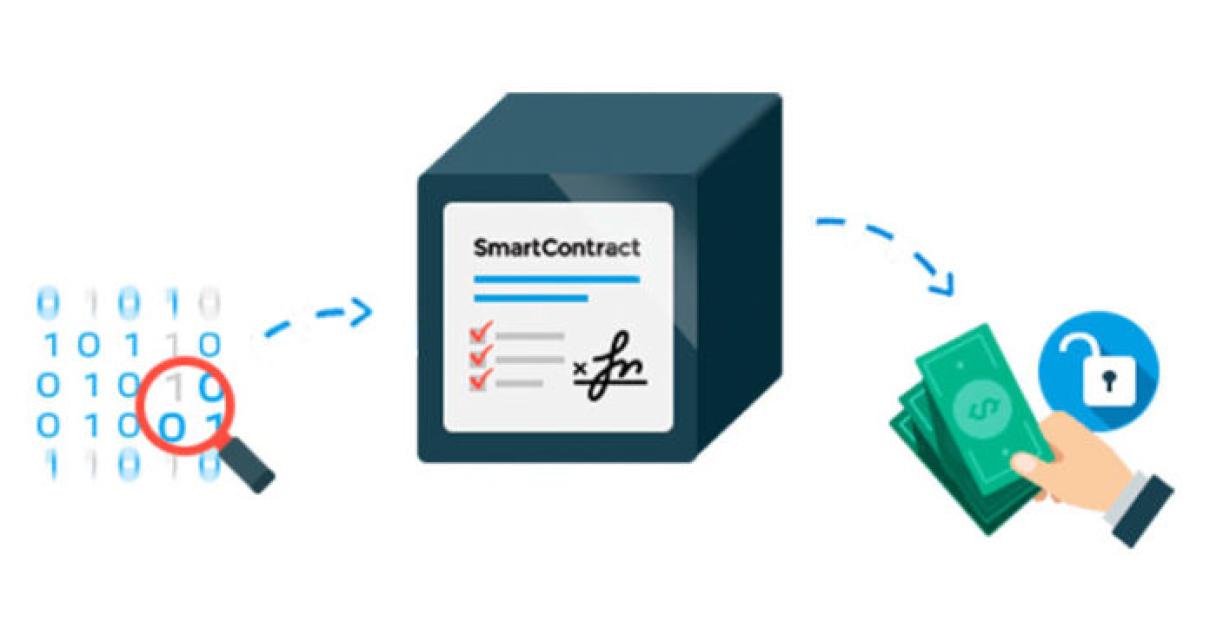

A smart contract is a digital contract that is executed and enforced by a network of connected nodes. It uses blockchain technology to create an immutable record of a contract between parties.

A blockchain is a distributed database that maintains a continuously growing list of updates to a contract. Each time a party to the contract makes a change, the blockchain updates the record to reflect the change. This ensures that the contract is always up-to-date and secure.

A smart contract can be used to create a variety of agreements, including contracts for goods and services, investments, and more. It can also be used to automate processes or enforce rules.

The potential applications of smart contracts in blockchain

technology are vast.

There are many potential applications of smart contracts in blockchain technology. Some of the most common applications of smart contracts include:

1. Contract management: Smart contracts can be used to manage and track the performance of contracts. This could be used, for example, to ensure that a contract is fulfilled.

2. Payment processing: Smart contracts can be used to process payments. This could be used, for example, to process payments between two parties who have agreed to a contract.

3. Asset management: Smart contracts could be used to manage assets. This could be used, for example, to manage property rights.

4. Crowdfunding: Smart contracts could be used to raise money through crowdfunding. This could be used, for example, to raise money for a new business idea.

5. Voting: Smart contracts could be used to vote on matters. This could be used, for example, to decide whether a new product should be released into the market.

The limitations of smart contracts in blockchain

The use of smart contracts in blockchain is a powerful tool for ensuring the integrity and enforceability of transactions. However, there are several limitations to the effectiveness of this technology.

First, smart contracts are not always compatible with the semantics of the blockchain network. For example, a smart contract that requires a specific blockchain version to operate may not be compatible with a network that is updated more frequently. This can result in unexpected or failed transactions.

Second, the enforcement of contract terms can be difficult. For example, if one party fails to meet their obligations under the contract, it may be difficult to compel them to do so. This can lead to contracts that are unenforceable or difficult to enforce.

Third, smart contracts are not immune to attack. Someone could attempt to tamper with or corrupt the code of a smart contract, causing it to fail or behave in an unintended way. This could have serious consequences for the parties involved in the contract.

Finally, there is a risk that blockchain technology may not be adopted by large businesses or governments. If this happens, smart contracts may not be as widely used as intended.